-

2022-03-15

CBDT issued Circular No. 3/2022 to clarify its position on

Mr. S.P. Singh (Ex-IRS & Ex-Senior Director, Deloitte) and Mr. Sharad Goyal (Founding Partner, GSAP & Associates LLP) discuss the concept of MFN, its applicability, controversies, finer points of the Circular and a few relevant decisions by various judicial authorities. Discussing the definition of MFN Clause, the authors highlight that that MFN Clause is not part of the OECD Model Convention however, finds place in the UN Manual for the Negotiation of Bilateral Tax Treaties between Developed and Developing Countries 2019. They opine that while the CBDT Circular intends to provide an understanding of how MFN Clause should apply and give clarity to the taxpayers, the issue regarding its applicability still remains as the Circular is binding on tax authorities but not on taxpayers thus, “the taxpayers can still resort to the judicial interpretation on this matter.”

The authors highlight that MFN Clause has gained prominence in the recent past following abolition of DDT. They discuss various decisions rendered on this matter and also the most recent Pune ITAT ruling in GRI Renewable Industries which specifically dealt with the applicability of the Circular. While signing off, the authors opine that “Going by the accepted legal process it is likely that other judicial authorities will be guided more by the preceding judicial decisions rather than the Circular.”

“CBDT Clarification on MFN Clause – Impact Analysis”

Arguably, Circular No. 3/2022 issued by the Central Board of Direct Tax (CBDT) on February 3, 2022, might have the unenviable distinction of being one of the few (if not the first) circular to have been knocked out by a judicial authority within the month of its issuance. The said circular seeks to clarify the position of the CBDT regarding the applicability of the Most-Favoured-Nation (MFN) clause of the Protocol to India’s Double Taxation Avoidance Agreements (DTAA) with several countries. The circular explains the circumstances under which the benefit of MFN clause could be availed by taxpayers. In this article the concept of MFN, its applicability, controversies, finer points of the Circular and a few relevant decisions by various judicial authorities are discussed.

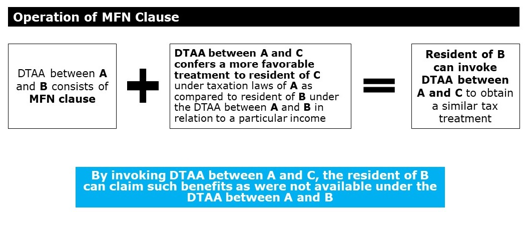

Let us first understand the MFN clause and its implications.

Meaning of MFN Clause

Black Law Dictionary (11th Edition) defines the term “Most Favoured Nation clause” to mean “in International investment law, a treaty clause guaranteeing that states will treat the other treat parties’ investors as favourably as they treat investors from any third state”. Thus, it can be said that, as the name suggests, MFN clause aims to extend certain preferential rights under one treaty to persons of another nation. Objective of MFN clause in bilateral treaties is to ensure that the contracting State is not treated less favourably than any other State under similar contracts which the first State may enter into. MFN is one step ahead of ‘non-discrimination clause’. Non-discrimination is aimed at removing discrimination between the nationals of two Contracting States only, whereas MFN clause removes discrimination viz-a-viz residents of a third State. Trade treaties and tax treaties frequently use MFN clause to boost economic relations amongst countries.

Normally, MFN clause may not apply to all streams of income and can be restricted only to defined types of income. Depending upon the language used in MFN clause, its application may be automatic (i.e., even if not specifically notified by the CBDT) or require the contracting States to renegotiate Tax Treaty.

It is interesting to note that MFN clause is not part of the OECD Model Convention. However, it is mentioned in the UN Manual for the Negotiation of Bilateral Tax Treaties between Developed and Developing Countries 2019 at paragraphs 119-121. It is explained that “the wording of these clauses, which are typically included in a protocol to the proposed treaty, varies in important ways. Some of these clauses provide that in such a case, the two countries will undertake negotiations with a view to modify the treaty so that the treaty partner is eventually granted the same benefit as that granted to the third country. In other cases, the effect of the clause is merely to require the two countries “to discuss” the granting of a similar benefit. Other clauses have a more direct and immediate impact and provide that a provision corresponding to the provision agreed to with the third country will automatically become applicable between the two countries as soon as the treaty with the third country enters into force. In addition, some of these clauses require the competent authority of the country that concludes a treaty with a third country that triggers the application of the clause to notify this fact to the competent authority of its treaty partner.”

All countries do not subscribe to inclusion of the MFN clause in their tax treaties. The UN advises that “if two countries agree to include a most favoured nation clause in a treaty, they should make it clear when that clause will be triggered (i.e. at the time of signature or entry into force of another treaty or when the provisions of that other treaty will become effective); when that clause will have effect (e.g. in the case of a clause that is intended to make a direct and immediate change to the rate of source taxation of dividends, what is the date from which dividends will benefit from that change) and, most importantly, what will be the effect of the clause (i.e. will the treaty be immediately amended and if yes, how; will the countries be required to conclude a protocol to change the treaty; will the change be implemented through another mechanism and if yes, which one; will the countries be merely required to enter into negotiation with the view of possibly making the change).”

The MFN clause, normally seek to extend lower rate of taxation in respect of dividends, interest, royalty as well as limit the scope of the definition or taxability. Further, the benefits are not extended to all treaty partners, but to a select group of countries.

MFN Clause in India’s DTAAs

MFN clause forms part of Protocol or Exchange of Letters to the DTAAs entered by India. Treaties with some OECD member States such as the Netherlands, France, the Swiss Confederation, Sweden, Spain and Hungry contain MFN clauses of varying scope in the Protocols to the concerned treaties. MFN clauses in the treaties of these States, inter alia, provide that if India enters into a treaty with another OECD State restricting the rate or/and scope of certain items of income (such as dividends, interest income, royalties, fees for technical services, etc.) then those beneficial provisions will be extended to the first mentioned country.

While reading MFN clause in Indian tax treaties one should look out for:

1. Reference made to the relevant convention, agreement, protocol?

2. Nature of income which the MFN clause relates to? Generally, MFN clause relates to royalties, fees for technical service (FTS), dividends and interest.

3. Benefit envisaged/provided? Rate or scope of definition or both, needs to be examined carefully.

4. Date of applicability of the MFN clause? Whether from the date of signing the treaty, or entry into force, or the effective date.

Let us try to understand how does MFN clause work. This has been nicely explained in a recent decision of the Income Tax Appellate Tribunal (ITAT)[1]. The DTAA in question was between India and Spain[2]. The decision has quoted paragraph 7 of the Protocol to the said DTAA as below:

‘7. The competent authorities shall initiate the appropriate procedures to review the provisions of Article 13 (Royalties and fees for technical services) after a period of five years from the date of its entry into force. However, if under any Convention or Agreement between India and a third State which is a Member of the OECD, which enters, into force after 1st January, 1990, India limits its taxation at source on royalties or fees for technical services to a rate lower or a scope more restricted than the rate or scope provided for in this Convention on the said items of incomes, the same rate or scope as provided for in that Convention or Agreement on the said items of income shall also apply under this convention with effect from the date on which the present Convention comes into force or the relevant Indian Convention or Agreement, whichever enters into force later.’

In view of the above a resident of Spain can claim benefit of a tax treaty between India and a third country, being member of OECD, which enters into force after 1st January 1990. Thus, while applying provisions of a DTAA one need to read not only the concerned DTAA but also any Protocol or Exchange of Letter to claim additional benefit. This would be subject to satisfaction of required conditions.

Circular No. 3/2022 issued by the CBDT on February 3, 2022

The Circular seeks to clarify that unilateral decree/bulletin/publication issued by the governments of treaty partner countries do not represent shared understanding of India on applicability of the MFN clause. In this connection it draws attention to the decree/bulletin/publication issued by the Netherlands, France and the Swiss Confederation wherein the beneficial rates of taxation on dividends provided in the treaty between India and Slovenia (which has become Member of the OECD after the concerned treaties were signed) has been claimed to be applicable to their residents due to the MFN clauses in their treaties with India. It is stated that both the Netherlands and France had passed their decree/bulletin without consulting India and hence do not share India’s stand. So far as the Swiss Confederation is concerned, India has clarified that the benefits of India's treaty with the third State cannot be imported into the India-Swiss treaty unless the third State was a member of the OECD at the time of signing that treaty.

As per CBDT, the MFN clause requires that for its applicability the third State must be a member of the OECD both at the time of conclusion of the treaty with India as well as at the time of applicability of MFN clause.

CBDT further clarifies that that the applicability of MFN clause and benefit of the lower rate or restricted scope of source taxation rights in relation to certain items of income (such as dividends, interest income, royalties, Fees for Technical Services, etc.) provided in India's treaties with the third States will be available to the first (OECD) State only when all the following conditions are met:

(i) The second treaty (with the third State) is entered into after the signature/ Entry into Force (depending upon the language of the MFN clause) of the treaty between India and the first State;

(ii) The second treaty is entered into between India and a State which is a member of the OECD at the time of signing the treaty with it;

(iii) India limits its taxing rights in the second treaty in relation to rate or scope of taxation in respect of the relevant items of income; and

(iv) A separate notification has been issued by India, importing the benefits of the second treaty into the treaty with the first State, as required by the provisions of sub-section (1) of section 90 of the Income Tax Act, 1961.

With the above clarifications, the CBDT has put forth its understanding of how MFN clause should apply and gave clarity to the taxpayers. But the question is does this really help? All issues regarding applicability of MFN are being litigated at various judicial levels. A Circular is binding on tax authorities and not on taxpayers. So, the taxpayers can still resort to the judicial interpretation on this matter.

Applicability of MFN clause became more important recently because India abolished Dividend Distribution Tax (DDT) w.e.f April 1, 2020 and dividend has become taxable in the hands of the shareholder. Since, the tax rate for dividend income under the domestic laws of India is 20% (plus applicable surcharge and cess), foreign shareholders of the Indian companies are now seeking shelter under the respective tax treaties for reducing tax liability in India on dividend income. Some of the tax treaties like with Slovenia, Colombia and Lithuania provides a low tax rate of 5% on dividend income.

Article 11 of the India-France treaty provides a rate of 10% on dividend income. Whereas Para 7 of the Protocol to the aforesaid Convention provides that:

“7. In respect of articles 11 (Dividends), 12 (Interest) and 13 (Royalties, fees for technical services and payments for the use of equipment), if under any Convention, Agreement or Protocol signed after 1-9-1989, between India and a third State which is a member of the OECD, India limits its taxation at source on dividends, interest, royalties, fees for technical services or payments for the use of equipment to a rate lower or a scope more restricted than the rate of scope provided for in this Convention on the said items of income, the same rate or scope as provided for in that Convention, Agreement or Protocol on the said items income shall also apply under this Convention, with effect from the date on which the present Convention or the relevant Indian Convention, Agreement or Protocol enters into force, whichever enters into force later.”

Article 10 of India-Slovenia treaty (effective from 17 February 2005), Article 10 of India-Lithuania treaty (effective from 10 July 2012) and Article 10 of India-Colombia treaty (effective from 7 July 2014) provides for tax rate of 5% on dividend income.

As it evident from discussion earlier, the Protocol to the India-France treaty includes an MFN clause, which means that favourable treatment accorded in a treaty with any other State which is a member of OECD should also apply to the tax residents of France. Slovenia, Lithuania and Columbia being member of the OECD, the benefits arising from the corresponding treaties of these countries with India, be extended to the India-France treaty, vide the above MFN clause, and accordingly a French taxpayer be able to take benefits of the reduced rates of tax on the dividends. This issue came up for consideration before the Hon’ble High Court of Delhi in the case of Steria (India) Ltd. vs. CIT [3].

In this case, pertaining to India-France treaty, the Income Tax Department contended that it is not permissible to rely upon one Convention between India and an OECD member State for the purposes of taking advantage of a lower rate of tax and then refer to another Convention to take advantage of a more restricted scope. Concluding that such restrictive interpretation cannot be upheld, the Hon’ble Delhi High Court stated that the words ‘a rate lower or a scope more restricted’ occurring therein envisages that there could be a benefit on either score i.e., a lower rate or more restricted scope. One does not exclude the other. The other expression used is ‘if any other Convention, Agreement or Protocol signed after 1-9-1989 between India and a third State which is a member of the OECD’. This also indicates that the benefit could accrue in terms of lower rate or a more restrictive scope under more than one Convention which may be signed after 1-9-1989 between India and a State which is an OECD member. The purpose of Clause 7 of the Protocol is to afford to a party to the India-France treaty the most beneficial of the provisions that may be available in another treaty between India and another OECD country.

Accordingly, the Court held that in view of clause 7 of the Protocol forming part of the India-France treaty, less restrictive definition of expression 'fees for technical services' appearing in the India-UK treaty, must be read as forming part of the India-France treaty as well. Hence, payment by an Indian company to a French company for management services would not constitute Fees for Technical Services under India-French treaty.

India-UK treaty entered into force in the year 1993 and UK is an OECD member country before this treaty was signed. Clause 7 of the Protocol to India-France treaty which provides for MFN benefit does put a condition that the third State person should be an OECD member, but it does not specify whether that person should be OECD member before signing of India-France treaty or Protocol or after that. Further, no condition is specified in Protocol to India-France treaty that a separate notification is required at India side to give effect to the benefits of the Protocol.

In the case of Steria (supra) the Hon’ble Delhi High Court held that clause 7 of the Protocol makes it self-operational. It is not in dispute that the India-France treaty was notified by the Central Government by issuing a notification under section 90. It is also not in dispute the separate Protocol signed between India and France simultaneously forms an integral part of the treaty itself. The preamble in the Protocol, which states 'the undersigned have agreed on the following provisions which shall form an integral part of the Convention', makes this position clear. Once the treaty has itself been notified, and contains the Protocol including para 7 thereof, there is no need for the Protocol itself to be separately notified or for the beneficial provisions in some other treaty between India and another OECD State to be separately notified to form part of the Indo-France treaty.

In another case of Poonawalla Aviation (P.) Ltd., In re [4], the Hon’ble AAR held that interest payable by an Indian company to French entities for providing export credit facility towards purchase of an aircraft is not taxable in India under Article 12.3(b) of India-France treaty in view of MFN clause in India-France Protocol. In this case it was argued that clause 7 of the Protocol makes it clear that if the taxation at source of interest income is limited by India in its treaty with another country after 1.9.1989 either by lowering the rate of tax or making the scope of taxation more restricted, the same benefit will also be available to the applicant. The applicant submitted that in treaties India had entered into with Canada, Hungary and Ireland exemption from taxation for interest relating to a loan or credit is available not only in respect of loans or credits made, guaranteed or extended, but also in respect of loans insured by certain institutions in France.

It may be noted that in this case the Hon’ble AAR relied upon the treaty with Hungary, which became a member of OECD in the year 1996 and India signed treaty with Hungary in the year 2005.

Benefit under the Protocol to the India-Swiss treaty were denied by the Assessing Officer (AO) in the case of Torrent Pharmaceuticals Ltd. vs. ITO [5]. Taxpayer was engaged in manufacturing of pharmaceutical products. During the financial year 2007-08 taxpayer remitted payments to overseas payees located in Switzerland for conducting tests for research. Assessing Officer held that remittances were in the nature of royalty/technical services. Appeal filed before the ITAT was to examine whether benefit of MFN clause is available to Swiss recipient and therefore, ‘make available’ restriction provided in the India-Portuguese tax treaty can apply to Swiss remittances. India-Swiss treaty entered into force in the year 1994. The erstwhile Clause 5 of Protocol between India and Switzerland with reference to Articles 10, 11 and 12 states that:

“If after the signature of the Protocol of 16th February, 2000 under any Convention, Agreement or Protocol between India and a third State which is a member of the OECD India should limit its taxation at source on dividends, interest, royalties or fees for technical services to a rate lower or a scope more restricted than the rate or scope provided for in this Agreement on the said items of income, then, Switzerland and India shall enter into negotiations without undue delay in order to provide the same treatment to Switzerland as that provided to the third State.”

ITAT held that India has entered into tax treaties with various countries viz., Netherlands, Sweden, France, Spain, Hungary, etc. which contain MFN clause and do not require India to re-negotiate the tax treaty. MFN clause in the Protocol to the India-Switzerland tax treaty provides that Switzerland and India shall enter into negotiations, subsequent to a more beneficial tax treaty entered into with other OECD country, in order to provide the benefit of reduced rate or restricted scope given in the subsequent tax treaty. So, unless India actually re-negotiates and approve the tax treaty, ‘make available’ clause under the India-Portuguese tax treaty cannot apply to India-Switzerland tax treaty. Portugal became OECD member in 1961 and the India-Portuguese Republic treated entered into force in the year 2000.

Reason for ITAT to deny benefit of MFN clause in this case was that the Protocol itself required renegotiation of the India-Swiss treaty post any other OECD member country treaty limiting scope of taxation of technical services then India and Switzerland Governments were to renegotiate tax treaty and at that point of time such a renegotiation did not happen, though it did happen in the year 2012. However, requirement of issue of circular by CBDT, as envisaged in February 3rd Circular, was examined by the ITAT in this case.

ITAT Decision in the Case of GRI Renewable Industries S. L.[6]

In this case the DTAA under consideration was between India and Spain and the MFN clause therein. The AO, in this case had denied the benefit of the India-Portugal DTAA to a resident of Spain on the ground that the Protocol was not notified by India.

The ITAT observed that a Protocol was an integral part of a tax treaty and once the “Agreement between India and Spain was notified on 21-04-1995, the Protocol, which is an integral part of the DTAA, also got automatically notified along with the Agreement”. Hence, it concluded that there was no need for a separate notification of the Protocol to import the MFN clause as has been made a condition in the above mentioned Circular. They also observed that once a DTAA is notified there is no need to separately notify parts of the DTAA.

So far as the applicability of the Circular is concerned the ITAT observes that “(I)t is a trite law that a circular issued by the CBDT is binding on the AO and not on the assessee or the Tribunal or other appellate authorities". They have gone on to reject the Circular, also, on the ground that it seeks to have a retrospective application which is not permissible. The basis for this observation is that “(I)t is a settled legal position that a piece of legislation which imposes a new obligation or attaches a new disability is considered prospective unless the legislative intent is clearly to give it a retrospective effect”.