-

2025-02-05

Analysis

Key Takeaways

• Delhi ITAT’s Ruling. What did the ITAT say in the first-ever application of Principal Purpose Test (PPT) in India?

• Insights from the Ruling. Did factors like diverse investments, business expenditure, and timing of incorporation help demonstrate that treaty benefit wasn’t the “principal purpose”?

• CBDT Circular. Followed the ITAT Ruling. Clarifies PPT applies prospective- ly; grandfathered investments are exempt; however, PPT requires an “objective assessment” of facts – how to grapple with it?

• Grandfathered and exempted – not entirely. Other forms of income such as NCD interest income, capital gains on debentures, derivatives, units of AIF / InvIT/ REIT continue to be subjected to PPT

• Mauritius – does it get a status lift?

Tax treaty benefits have been extensively litigated in India. Not too long ago, the tax department had retrospectively reopened assessments of several global investors and slapped substantial tax demands alleging that these entities had indulged in tax evasion by treaty shopping. While courts have consistently upheld[1] tax residency certificates (TRC) as sufficient proof of residency (and that the tax department cannot go behind a TRC to question an entity’s residential status), the tax department continues to scrutinize bonafide offshore structures. With the incorporation of anti- abuse measures like PPT and the general anti-avoidance rules (GAAR) in the Income-tax Act (ITA), this scrutiny has only intensified.

Now, in a first of its kind ruling[2], the Delhi ITAT has applied PPT and allowed treaty benefits for Indian income after considering the taxpayers’ structure and activities. Shortly after this ruling, the CBDT via a circular (Circular) clarified PPT’s applicability and its interplay with grandfathered investments. In this piece, we discuss the following:

1. What is PPT? Has it shifted the burden of proof on the taxpayer?

2. Lessons from SC Lowy – How to demonstrate treaty benefit wasn’t the “principal purpose”?

3. CBDT’s guidance – What is it and who is it really benefitting?

4. GAAR – PPT interplay

5. Factors you must consider when choosing your investing jurisdiction

6. Mauritius v. Singapore – does the once favoured jurisdiction get a second look?

7. What happens to income from NCDs, capital gains from indirect transfers, REITs and InvITs?

What is PPT?

It is a general anti-abuse rule which allows the tax authorities to deny treaty benefits if one of the principal purposes of a transaction/ arrangement is to obtain tax benefit. The taxpayer, however, can still avail the benefits it they can prove that obtaining the benefit was in accordance with the object and purpose of the treaty. The provision is reproduced below:

“7. Notwithstanding the other provisions of this Convention, a benefit under this Convention shall not be granted in respect of an item of income or capital if it is reasonable to conclude, having regard to all relevant facts and circumstances, that obtaining that benefit was one of the principal purposes of any arrangement or transaction that resulted directly or indirectly in that benefit, unless it is established that granting that benefit in these circumstances would be in accordance with the object and purpose of the relevant provisions of this Convention.”

Has PPT shifted the burden of proof?

Yes. Once the tax authority comes to a reasonable conclusion that one of the principal purposes was to take treaty benefit, it’s on the taxpayer to “establish” that the benefit was “in accordance with the object and purpose” of the treaty. To do so, the taxpayer must bring on record concrete evidence. Bottomline, the burden of proof squarely rests on the taxpayer to demonstrate that the arrangement for which benefit is sought was in accordance with the treaty. The requirement on the authority’s behalf is a low threshold since the tax authority is only required to arrive at a reasonable conclusion and not factually prove its case.

How did PPT come about?

In response to the 2008 financial crisis, the OECD initiated the Base Erosion and Profit Shifting (BEPS) project in 2013 to address loopholes in the international tax framework. One of the key outcomes of this project was the introduction of PPT, which focused on preventing treaty abuse. Cognizant of the fact that bilaterally negotiating amending protocols would be a cumbersome process; OECD came with the Multilateral Convention to Implement Tax Treaty Related Measures to Prevent BEPS (MLI). The MLI effectively modifies almost 2,000 existing tax treaties worldwide to close opportunities for tax avoidance. The mechanism of MLI is detailed in Annexure – A. Specifically, Article 7 of the MLI lays down PPT. With India ratifying the MLI in 2019, the PPT was successfully incorporated into India’s tax treaty network.

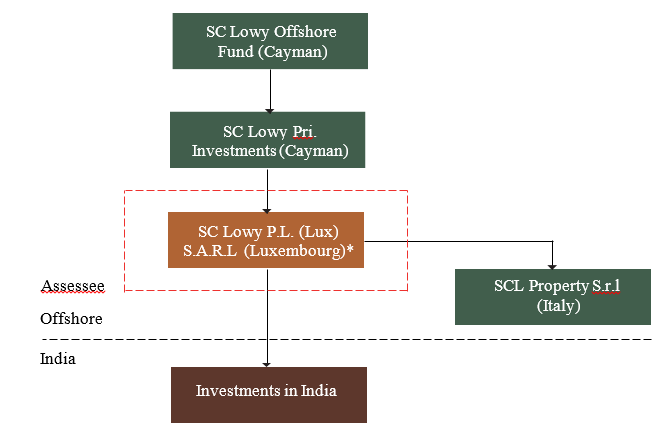

SC Lowy Ruling: Factors that turned the case

From theory to practice, the Delhi ITAT ruling became India’s first application of PPT. The assessee, a Luxembourg entity with a foreign portfolio investor license, was structured as a step- down subsidiary of a Cayman Islands parent.

*14% of the assessee’s portfolio comprised of India investments

The assessing officer denied treaty benefits citing the following grounds (without substantiating):

a. Assessee was not the beneficial owner of the income – real owner was its holding company in Cayman Islands;

b. Assessee was a conduit entity;

c. TRC is not sufficient to establish tax residency (and avail treaty benefits) if the entity lacks economic substance; and

d. There was no commercial rationale for establishment in Luxembourg – done merely to take benefit of the DTAA as India does not have a tax treaty with Cayman Islands.

On appeal, the ITAT set aside the assessing officer’s order and allowed the treaty benefits. Drawing from precedents like Vodafone[3] and Tiger Global[4], the Tribunal upheld the sufficiency of the TRC and reiterated that the tax department cannot go behind a TRC except in limited circumstances[5]. Even in such scenarios, mere suspicion cannot invalidate treaty benefits and the tax department is required to discharge a high burden of proof by bringing on record “cogent and convincing” evidence.

The ITAT does not interpret/ elaborate on PPT. But it does appreciate certain facts which lead it to conclude that the assessee was not set up in Luxembourg with the principal purpose of obtaining treaty benefits. The ITAT’s acceptance of these factors provides guidance to offshore entities facing revenue scrutiny for their jurisdictional choices. It appears that the ITAT was convinced of the genuineness and commercial substance of the assessee by virtue of the following key facts:

a. ~86% investments in jurisdictions other than India;

b. existence prior to first India investment;

c. filed tax returns and paid tax in Luxembourg on its worldwide income;

d. substantial operational expenditure; and

e. control over the use of funds and absence of an obligation to upstream to its Cayman parent.

CBDT’s Guidance on PPT: Muddies the treaty waters

Roughly 3 weeks after the Delhi ITAT ruling, the CBDT issued the Circular providing guidance on how PPT is to be applied in the context of India’s tax treaties.

At the outset, the Circular notes that PPT is intended to ensure that treaty benefits are only granted for bonafide transactions, and its application requires an “objective assessment of the relevant facts and circumstances”. What is an “objective assessment” is left open. It then clarifies the following:

a. Prospective application. PPT will only apply prospectively[6].

b. Grandfathered structures. India’s treaties with Mauritius, Singapore, and Cyprus contain specific bilateral commitments to grandfather investments. PPT won’t apply to investments under these treaties. The specific provisions in these treaties (e.g. limitation of benefits) will apply. A scenario analysis of the interplay between grandfathered investments and PPT is in Annexure – B.

c. Supplementary guidance. Application of PPT requires a “context-specific fact-based” assessment. Tax department can resort to the BEPS Action Plan 6 Report[7] and the UN Model Tax Convention Commentary[8] for supplementary guidance.

Circular’s hits and misses

Keeping grandfathered structures outside the purview of PPT is an important clarification, since such structures continue to face tax department’s scrutiny on various grounds. To that extent, this Circular should reduce, if not quell, demands in respect of income from transfer of pre-2017 equity investments.

But nudging revenue officers to rely on supplementary sources like the action plan report could yield mixed outcomes. While these sources do provide (marginally) clearer guidelines for identifying when scrutiny of a particular arrangement is warranted, they also include a list of “illustrations” which could muddy the waters while interpreting and applying PPT.

It would have been more useful if the Circular gave specific examples, or at the least, clear criteria for when PPT would not apply, instead of relying on case-by-case assessments.

Lessons from Australia

The CBDT could take a leaf from the Australian tax department’s Law Administration Practice Statement[9] (LAPS) on applying PPT. The LAPS on application of PPT provides a structured framework, which involves framing questions to determine the purpose of an arrangement, such as the broader business context, the arrangement’s results, its terms, existence of an alternative arrangement to achieve non-tax objectives, and the non-tax benefits driving its implementation etc[10]. By incorporating such clear guidelines, one can ensure an objective assessment while also affording a certain degree of flexibility to the tax authorities.

Despite not having clear guidelines, on balance, we believe that the Circular offers some indication on how the tax department views PPT. One thing is clear – while applying PPT, the tax department must examine whether the arrangement aligns with the primary objective of the treaty i.e. promoting genuine trade and capital movement.

Who benefits from the CBDT Circular – and who doesn’t?

The Circular provides a clear advantage to grandfathered investments, as they are exempt from the application of PPT. However, it is important to note that only pure equity investments from Mauritius and Singapore have been grandfathered. Other forms of investments and their corresponding income – such as interest income, capital gains from the sale of AIF or infrastructure trust units, derivatives, or the sale of equity shares in a foreign company holding a substantial interest in an Indian entity – will now be subject to the PPT.

Mauritius currently imposes a 7.5% withholding tax on interest income from India, compared to Singapore’s 15%[11]. Although Mauritius once fell out of favor due to concerns about commercial substance, it now appears to hold a slight advantage, at least in principle, because it has not yet adopted PPT. Of course, demonstrating genuine commercial substance remains critical; however, in the absence of PPT, Mauritius may now get a second look. In the long run, we anticipate that Mauritius will also adopt the PPT.

GAAR v. PPT: What’s the difference?

Vis-à-vis PPT, GAAR provisions under ITA are much narrower. The test for PPT is “one of the principal purposes” (as opposed to the “main purpose” under GAAR). Obtaining a treaty benefit doesn’t have to be the only or main reason for a transaction. Other reasons can be involved too. However, if getting the benefit is a key purpose and the treaty wasn’t meant to grant it, the tax authorities can deny the benefit.

On the other hand, GAAR is narrower. 2 conditions must be met:

a. the ‘main purpose’ of the arrangement is to obtain tax benefit; and

b. the arrangement satisfies other tests like arms’ length test, commercial substance test, bonafide purpose test or doesn’t result in the misuse/ abuse of the ITA.

In this backdrop, can the tax department can go after the grandfathered equity investments under GAAR? The answer is no. The law prescribes that GAAR provisions do not apply to any income arising from transfer of investments made on or before April 01, 2017[12]. However, for any investments (equity or otherwise) made after April 01, 2017, but before PPT comes into effect, the tax department could still invoke GAAR and deny treaty benefits. Needless to say, PPT will prospectively apply from the date it is notified.

Conclusion

With introduction of PPT and GAAR, the scope for scrutiny over offshore structures has only increased. In this context, the Circular’s clarifications regarding prospective application and exclusion of grandfathered structures from PPT’s purview are positive developments. However, challenges remain, on account of lack of clear, structured guidelines on how PPT should apply. Bottomline, till such time there are clear guidelines in place, taxpayers coming from tax-friendly jurisdictions may continue to face denial of treaty benefits under PPT.

Annexure – A: How does MLI work?

• The MLI applies to “Covered Tax Agreements” (CTAs). For a tax agreement to be covered by the MLI, each participating country must notify the OECD of the specific bilateral income tax treaties it wishes to designate as CTAs.

• Then, that country designates which provisions of the MLI it wishes to adopt for each CTA. Some provisions, known as minimum standards, must be adopted, while others are optional.

• If both parties to a bilateral tax agreement designate it as such, it becomes a CTA, and the MLI will modify the agreement.

Annexure – B: Impact of the CBDT Circular on key treaties

a. India – Singapore Treaty

• PPT comes into effect from FY 2020-21.

• The grandfathering benefit under the treaty is subject to satisfaction of the LOB clause (i.e. should not be a shell/ conduit company by meeting minimum expenditure test). In addition to the PPT and satisfying the conditions re. shell/ conduit entities, the treaty also has a general clause which denies the capital gains tax benefit if the affairs are arranged with the ‘primary purpose’ of obtaining that benefit – much narrower than the PPT. This means that even if PPT does not apply, the LOB provision can be used to deny the benefit if the primary purpose of the arrangement is to obtain a tax benefit.

|

Instrument |

Acquisition Date |

Transfer Date |

PPT Applicability |

|

Shares |

Before April 01, 2017 |

Irrespective of transfer date |

N/A |

|

After April 01, 2017 |

Before April 01, 2020 |

N/A |

|

|

After April 01, 2017 |

After April 01, 2020 |

Applicable |

|

|

Other than shares |

Before April 01, 2017 |

Before April 01, 2020 |

N/A |

|

Before April 01, 2017 |

After April 01, 2020 |

Applicable |

b. India – Mauritius Treaty

• ° Though the protocol introducing PPT has not been notified yet, the Circular makes it clear that PPT will not apply to the grandfathered investments. Once the protocol is notified, PPT should apply to provisions of India-Mauritius tax treaty.

• ° Importantly, the treaty does not have a general LOB clause[13], therefore, PPT will act as the only anti-abuse measure.

Annexure – C: Withholding rates under the Mauritius & Singapore Treaty

|

Jusrisdiction |

WHT Rates |

|||

|

|

Interest |

Dividend |

Royalties |

FTS |

|

Mauritius |

7.5[14] |

5[15]/15 |

15 |

10 |

|

Singapore |

10[16]/15 |

10[17]/15 |

10 |

10 |

[1] Blackstone Capital Partners (Singapore) VI FDI Three Pte. Ltd. v. Assistant Commissioner of Income Tax, Delhi, [TS-6258-HC-2023(Delhi)-O]

[2] S.C. Lowy P.I. (Lux) S.A.R.L. v. ACIT, [TS-972-ITAT-2024(DEL)]

[5] Tax fraud, sham transactions, attempts to conceal illegal activities, or the complete absence of economic substance.

[6] In cases where PPT was bilaterally negotiated (eg. China, Hong Kong), PPT would apply from the date of entry into force of the tax treaty or the amending protocol incorporating PPT. On the other hand, in cases where PPT was incorporated through MLI, the entry into effect would depend on when the contracting state deposits the ratification instrument..

[7] The report can be accessed here.

[8] Commentary of Art. 1 and Art. 29, UN Model Tax Convention.

[9] LAPS is published with the same objective as CBDT circulars – guide the officers administering tax laws. LAPS contain a set of instructions to tax officers and provides direction and assistance on how the approach while applying the Australian tax laws.

[10] The detailed list of questions and considerations can be found here.

[11] A detailed comparison of the withholding rates for different incomes is in Annexure - C.

[12] Rule 10U, Income-tax Rules, 1961.

[13] Rule 10U, Income-tax Rules, 1961.

[14] Taxable in the country of source as per domestic tax rates.

[15] If at least 10% of capital is owned by the beneficial owner (company) of the company paying the dividend.

[16] If paid on a loan granted by a bank/financial institution.

[17] If at least 25% of capital is owned by the beneficial owner (company) of the company paying the dividend.