-

2017-05-29

The Finance Act 2017 introduced section 50CA and clause (x) to section 56(2) in the Income Tax Act, 1961 (‘IT Act’) w.e.f. 1 April, 2017, to deal with specified transactions undertaken at a value below the fair market value computed as per prescribed guidelines (‘FMV’). Broadly, section 50CA of the IT Act deems FMV to be the sales consideration for computing capital gains on transfer of unquoted shares and section 56(2)(x) of the IT Act deems difference between the FMV and the transaction value in case of receipt of properties (including shares, immovable property, etc.) to be income in the hands of the recipients.

On 5th May, 2017, Central Board of Taxes (‘CBDT’) published the much awaited draft rules for sections 50CA and 56(2)(x) of the IT Act, to substitute existing rules as set out in rule 11UA of the Income Tax Rules, 1962 (‘IT Rules’) for computing FMV of unquoted shares. In this article, the author intends to dissect the draft rules, discuss the interplay between the two sections and highlight the key challenges arising therefrom particularly in connection with unquoted shares.

I. Whether the draft rules shift the valuation approach from book value to market value?

Existing rules prescribe book value of unquoted shares as on the transaction date (‘Valuation Date’) to be the FMV of such shares. The memorandum explaining the Finance Bill, 2017 suggests that the intention to replace the existing provisions was to collect fair share of taxes where unquoted shares are transferred at “understated” value by the transferor and received by the transferee for inadequate consideration. Keeping in view this objective, the draft rules propose to expand the scope of rule 11UA(1)(c)(b) of the IT Rules to compute the FMV of unquoted shares on the basis of the following formula:

FMV = (A+B+C+D-L) x (PV)/(PE)

Broadly, “A+B+C+D-L” in the above formula is the sum total of the following:

(a) net book value of all assets less liabilities [excluding book value of jewellery, artistic work, shares and securities and immovable property (‘Specified Assets’)]; plus

(b) market value of jewellery and artistic work as certified by a registered valuer; plus

(c) market value of shares and securities computed as per the valuation guidelines prescribed in rule 11UA (i.e. quoted shares – based on exchange traded price and unquoted shares – reusing the same formula as above); plus

(d) stamp duty value of immovable property.

PV = paid up value of equity shares;

PE = total amount of paid up equity share capital as shown in the balance-sheet.

The inclusion of FMV/stamp duty value of the underlying Specified Assets in computing the FMV of unquoted shares would now bring in parity in taxation whether Specified Assets are transferred directly or indirectly (i.e. by way of transfer of shares of the holding company which houses such assets). Thus, the above methodology will help to curb widely used practice of transfer of Specified Assets indirectly through medium of transfer of shares.

Nonetheless, the rule still focuses on “book value” of the company (except for Specified Assets) without giving due consideration to other factors relevant for business valuation and thus, leaving out several transactions out of its ambit. For instance, the draft rules may not materially impact transfer of “unquoted shares” of a service company – where the key drivers are intangibles (business intangibles and /or personnel intangibles) which are generally not captured in the books of accounts. As against this, if the shares of the same service company were “quoted”, the FMV being exchange traded price of such shares is likely to capture all business aspects (including intangibles, future earnings, etc.). Thus, in the author’s view, the rules for valuation of unquoted shares have merely shifted from the concept of book value to a so called adjusted book value concept and not to reflect “fair” market value.

As an alternate to the draft rules, value under discounted free cash flow method combined with FMV of jewellery and artistic work and stamp duty value of immovable property or any other internationally accepted method may be considered. Although these methods may entail a certain degree of subjectivity, they may better achieve the intended objective.

II. Interplay between sections and rules leading to a “double whammy”:

FMV of unquoted shares computed as per the draft rule 11UA(1)(c)(b) of the IT Rules is proposed to be applicable for both the sections, i.e. section 56(2)(x) and section 50CA of the IT Act. As a result, where unquoted shares are transferred at a value below the FMV, the difference between the FMV and the transaction value will get taxed twice – firstly, as capital gains in the hands of the transferor in view of section 50CA of the IT Act and secondly, as income from other sources in the hands of the recipient in view of section 56(2)(x) of the IT Act. Similar double taxation would also arise in case of transfer of immovable property at a value below its stamp duty valuation in view of simultaneous operation of section 50C of the IT Act in the hands of the transferor and section 56(2)(x) of the IT Act in the hands of the recipient.

While there is no doubt that the Government has all the power to levy and recover fair share of their taxes, double taxation of the same transaction – though in the hands of different taxpayers is completely unjustified. Accordingly, appropriate amendments need to be made in these sections to do away with the double whammy implications. The Government ought to make a choice between taxing such transactions either under capital gains provisions or income from other sources. The author has attempted below to explain the basis for such choice.

Transfer of capital assets is a transaction that technically falls with the ambit of capital gains and thus, subjecting it to the provisions of section 50C and 50CA of the IT Act would ensure that the differential amount is also taxed at the right tax bracket – for instance in case of long term capital gains, the differential amount will also get taxed at the rate of 20%. In contrast to this, in the same situation if the differential amount is subjected to the provisions of section 56(2)(x) of the IT Act, the applicable tax rate would become 30% or slab rates in case of resident taxpayer. To address this situation, the option to exclude those transactions which get covered within the ambit of section 50C and 50CA of the IT Act and accordingly suffer capital gains tax from the purview of section 56(2)(x) of the IT Act could be explored. Corresponding amendment to section 49 of the IT Act may also be required to link the cost of acquisition in the hands of the recipient to section 50C and 50CA of the IT Act.

In the absence of any amendment, to avoid such double tax implications, all transaction for unquoted shares and immovable property would mandatorily have to be undertaken at or above FMV, even though transacting at lower value could be otherwise justified.

III. Clarifications required in the valuation rules:

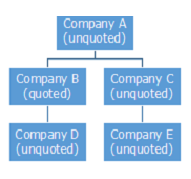

To better understand the issues to be discussed in this section, we will take help of the following illustration. The group structure of Company A which inter-alia has made investments in quoted and unquoted shares is set out below:

If shares of Company A are proposed to be transferred by its shareholders, the provisions of both section 50CA and 56(2)(x) of the IT Act will kick in. For this purpose, the draft valuation rules provide that for computing FMV of shares of Company A, market value of shares of investee companies (i.e. Company B and Company C) would also have to be computed in accordance with rule 11UA. While this appears to be conceptually fair and just, the following points in this connection need additional consideration:

- Valuation of quoted shares:

In our illustration, shares of Company B that are quoted on recognized stock exchange is to be valued in accordance with rule 11UA (1)(c)(a) of the IT Rules. In essence, the said rule provides that FMV of quoted shares is the exchange traded price as on the Valuation Date. However, a closer look at the language of the rule, indicates that the rule operates only in those cases where the shares are “received as on the Valuation Date”. Since the shares of Company B are not acquired by Company A on the Valuation Date, although the intention of the Government is quite clear, a strict reading of provisions could make rule 11UA(1)(c)(a) of the IT Rules inapplicable for computing FMV of shares of Company B as on the Valuation Date.

Further, since the market value of shares of Company D would already be captured in the price at which the shares of Company B are traded in the stock exchange, separate valuation of shares of Company D as on the Valuation Date should not be required.

Appropriate amendments to the language of the rule should help in avoiding unnecessary litigation.

- Valuation of unquoted shares:

- Reference to balance-sheet in the rules:

The existing rule 11UA(1)(c)(b) of the IT Rules which deal with valuation of unquoted shares, links the valuation to book value of Assets (‘A’), Liabilities (‘L’) and Paid-up Equity share (‘PE’) as stated in the “balance-sheet”. For this purpose, rule 11U(b) of the IT Rules requires balance sheet of the company to be drawn up as on the Valuation Date and audited by the statutory auditor.

The draft rule 11UA(1)(c)(b) of the IT Rules has deleted the reference to the term “balance-sheet” in defining A and L, but continued its reference in definition of PE. This makes it unclear as to whether under new rules the requirement to get balance-sheet audited as on the Valuation Date still exists. Where the answer to this is positive, the related question that arises is whether such requirement applies only to the company whose shares are being transferred, in the instant case Company A or also to the investee companies shares of which are unquoted (in the instant case Company C and Company E also). There may be practical challenges in getting audited balance sheets as on the Valuation Date of investee companies especially in cases where the shareholders have minority stake in those companies. As an alternative, linking the valuation of Company B and Company C to the last audited balance sheet could be considered.

- Cross holding situations:

Valuation of unquoted shares in situations where the group structure involves cross holding or circular holding of shares between the group companies may become difficult (or impossible!) as the values in such cases may get interlocked.

In a nutshell, in light of the various technical and practical aspects involved, one can only be hopeful that before issuing the final guidelines, CBDT will give a second eye to the draft rules and the interplay between the various sections involved. In the absence of relevant amendments, the tax payers could suffer double taxation on transactions involving sale of unquoted shares and immovable properties and in the long run would only lead to litigations.