-

For support, write to us on: admin@taxsutra.com

- Register

- Login

Latest News

Ministry of Finance

ECONOMIC SURVEY 2022-23: HIGHLIGHTS

Indian economy staging a broad based recovery across sectors, positioning to ascend to pre-pandemic growth path in FY23

Retail inflation is back within RBI's target range in November 2022

Direct Tax collections for the period April-November 2022 remains buoyant

Enhanced Employment generation seen in the declining urban unemployment rate and in the faster net registration in Employee Provident Fund

Creating public goods to enhance opportunities, efficiencies and ease of living, trust-based governance, enhancing agricultural productivity and promoting the private sector as a co-partner in development is the focus of the government reforms

Cleaner balance sheets led to enhanced lending by financial institutions

Growth in credit offtake, increased private capex to usher virtuous investment cycle

Non-food credit offtake by Scheduled Commercial Banks growing in double digits since April 2022

Gross Non-Performing Assets (GNPA) ratio of SCBs has fallen to a seven-year low of 5.0

Social sector expenditure (Centre and States combined) increases to Rs. 21.3 lakh crore in FY23 (BE) from Rs. 9.1 lakh crore in FY16

Central and State Government’s budgeted expenditure on health sector touched 2.1% of GDP in FY23 (BE) and 2.2% in FY22 (RE) against 1.6% in FY21

More than 220 crore COVID vaccine doses administered

Survey highlights the findings of the 2022 report of the UNDP on Multidimensional Poverty Index which says that 41.5 crore people exit poverty in India between 2005-06 and 2019-20

India declared Net Zero Pledge, to achieve net zero emissions goal by 2070

A mass movement LIFE– Life style for Environment launched

National Green Hydrogen Mission to enable India to be energy independent by 2047

Private investment in agriculture increases to 9.3% in 2020-21

Free foodgrains to about 81.4 crore beneficiaries under the National Food Security Act for one year

About 11.3 crore farmers were covered under PM KISAN in its April-July 2022-23 payment cycle

India stands at the forefront to promote millets through the International Year of Millets initiative

Investment of ₹47,500 crores under the PLI schemes in FY22- 106% of the designated target for the year

India’s e-commerce market is projected to grow at 18 per cent annually through 2025

Merchandise exports of US$ 332.8 billion for April-December 2022

India is the largest recipient of remittances globally receiving US$ 100 billion in 2022

PM GatiShakti National Master Plan creates comprehensive database for integrated planning and synchronised implementation across Ministries/ Departments

UPI-based transactions grew in value (121 per cent) and volume (115 per cent) terms, between 2019-2022, paving the way for its international adoption

Dated: 31 JAN 2023

Union Minister for Finance and Corporate Affairs, Smt. Nirmala Sitharaman, presented the Economic Survey 2022-23 in the Union Parliament today. The highlights of the Survey are as follows:

State of the Economy 2022-23: Recovery Complete

- Recovering from pandemic-induced contraction, Russian-Ukraine conflict and inflation, Indian economy is staging a broad based recovery across sectors, positioning to ascend to the pre-pandemic growth path in FY23.

- India's GDP growth is expected to remain robust in FY24. GDP forecast for FY24 to be in the range of 6-6.8 %.

- Private consumption in H1 is highest since FY15 and this has led to a boost to production activity resulting in enhanced capacity utilisation across sectors.

- The Capital Expenditure of Central Government and crowding in the private Capex led by strengthening of the balance sheets of the Corporates is one of the growth driver of the Indian economy in the current year.

- The credit growth to the MSME sector was over 30.6 per cent on average during Jan-Nov 2022.

- Retail inflation is back within RBI's target range in November 2022.

- Indian Rupee performed well compared to other Emerging Market Economies in Apr-Dec2022.

- Direct Tax collections for the period April-November 2022 remain buoyant.

- Enhanced Employment generation seen in the declining urban unemployment rate and in the faster net registration in Employee Provident Fund.

- Economic growth to be boosted from the expansion of public digital platforms and measures to boost manufacturing output.

India’s Medium Term Growth Outlook: with Optimism and Hope

- Indian economy underwent wide-ranging structural and governance reforms that strengthened the economy's fundamentals by enhancing its overall efficiency during 2014-2022.

- With an underlying emphasis on improving the ease of living and doing business, the reforms after 2014 were based on the broad principles of creating public goods, adopting trust-based governance, co-partnering with the private sector for development, and improving agricultural productivity.

- The period of 2014-2022 also witnessed balance sheet stress caused by the credit boom in the previous years and one-off global shocks, that adversely impacted the key macroeconomic variables such as credit growth, capital formation, and hence economic growth during this period.

- This situation is analogous to the period 1998-2002 when transformative reforms undertaken by the government had lagged growth returns due to temporary shocks in the economy. Once these shocks faded, the structural reforms paid growth dividends from 2003.

- Similarly, the Indian economy is well placed to grow faster in the coming decade once the global shocks of the pandemic and the spike in commodity prices in 2022 fade away.

- With improved and healthier balance sheets of the banking, non-banking and corporate sectors, a fresh credit cycle has already begun, evident from the double-digit growth in bank credit over the past months.

- Indian economy has also started benefiting from the efficiency gains resulting from greater formalisation, higher financial inclusion, and economic opportunities created by digital technology-based economic reforms.

- Thus Chapter 2 of the Survey shows that India's growth outlook seems better than in the pre-pandemic years, and the Indian economy is prepared to grow at its potential in the medium term.

Fiscal Developments: Revenue Relish

- The Union Government finances have shown a resilient performance during the year FY23, facilitated by the recovery in economic activity, buoyancy in revenues from direct taxes and GST, and realistic assumptions in the Budget.

- The Gross Tax Revenue registered a YoY growth of 15.5 per cent from April to November 2022, driven by robust growth in the direct taxes and Goods and Services Tax (GST).

- Growth in direct taxes during the first eight months of the year was much higher than their corresponding longer-term averages.

- GST has stabilised as a vital revenue source for central and state governments, with the gross GST collections increasing at 24.8 per cent on YoY basis from April to December 2022.

- Union Government's emphasis on capital expenditure (Capex) has continued despite higher revenue expenditure requirements during the year. The Centre's Capex has steadily increased from a long-term average of 1.7 per cent of GDP (FY09 to FY20) to 2.5 per cent of GDP in FY22 PA.

- The Centre has also incentivised the State Governments through interest-free loans and enhanced borrowing ceilings to prioritise their spending on Capex.

- With an emphasis on infrastructure-intensive sectors like roads and highways, railways, and housing and urban affairs, the increase in Capex has large-scale positive implications for medium-term growth.

- The Government’s Capex-led growth strategy will enable India to keep the growth-interest rate differential positive, leading to a sustainable debt to GDP in the medium run.

Monetary Management and Financial Intermediation: A Good Year

- The RBI initiated its monetary tightening cycle in April 2022 and has since raised the repo rate by 225 bps, leading to moderation of surplus liquidity conditions.

- Cleaner balance sheets led to enhanced lending by financial institutions.

- The growth in credit offtake is expected to sustain, and combined with a pick-up in private capex, will usher in a virtuous investment cycle.

- Non-food credit offtake by scheduled Commercial Banks (SCBs) has been growing in double digits since April 2022.

- Credit disbursed by Non-Banking Financial Companies (NBFCs) has also been on the rise.

- The Gross Non-Performing Assets (GNPA) ratio of SCBs has fallen to a seven-year low of 5.0.

- The Capital-to-Risk Weighted Assets Ratio (CRAR) remains healthy at 16.0.

- The recovery rate for the SCBs through Insolvency and Bankruptcy (IBC) was highest in FY22 compared to other channels.

Prices and Inflation: Successful Tight-Rope Walking

- While the year 2022 witnessed a return of high inflation in the advanced world after three to four decades, India caps the rise in prices.

- While India’s retail inflation rate peaked at 7.8 per cent in April 2022, above the RBI’s upper tolerance limit of 6 per cent, the overshoot of inflation above the upper end of the target range in India was however one of the lowest in the world.

- The government adopted a multi-pronged approach to tame the increase in price levels

- Phase wise reduction in export duty of petrol and diesel

- Import duty on major inputs were brought to zero while tax on export of iron ores and concentrates increased from 30 to 50 per cent

- Waived customs duty on cotton imports w.e.f 14 April 2022, until 30 September 2022

- Prohibition on the export of wheat products under HS Code 1101 and imposition of export duty on rice

- Reduction in basic duty on crude and refined palm oil, crude soyabean oil and crude sunflower oil

- The RBI’s anchoring of inflationary expectations through forward guidance and responsive monetary policy has helped guide the trajectory of inflation in the country.

- The one-year-ahead inflationary expectations by both businesses and households have moderated in the current financial year.

- Timely policy intervention by the government in housing sector, coupled with low home loan interest rates propped up demand and attracted buyers more readily in the affordable segment in FY23.

- An overall increase in composite Housing Price Indices (HPI) assessment and Housing Price Indices market prices indicates a revival in the housing finance sector. A stable to moderate increase in HPI also offers confidence to homeowners and home loan financiers in terms of the retained value of the asset.

- India’s inflation management has been particularly noteworthy and can be contrasted with advanced economies that are still grappling with sticky inflation rates.

Social Infrastructure and Employment: Big Tent

- Social Sector witnessed significant increase in government spending.

- Central and State Government’s budgeted expenditure on health sector touched 2.1% of GDP in FY23 (BE) and 2.2% in FY22 (RE) against 1.6% in FY21.

- Social sector expenditure increases to Rs. 21.3 lakh crore in FY23 (BE) from Rs. 9.1 lakh crore in FY16.

- Survey highlights the findings of the 2022 report of the UNDP on Multidimensional Poverty Index which says that 41.5 crore people exit poverty in India between 2005-06 and 2019-20.

- The Aspirational Districts Programme has emerged as a template for good governance, especially in remote and difficult areas.

- eShram portal developed for creating a National database of unorganised workers, which is verified with Aadhaar. As on 31 December 2022, a total of over 28.5 crore unorganised workers have been registered on eShram portal.

- JAM (Jan-Dhan, Aadhaar, and Mobile) trinity, combined with the power of DBT, has brought the marginalised sections of society into the formal financial system, revolutionising the path of transparent and accountable governance by empowering the people.

- Aadhaar played a vital role in developing the Co-WIN platform and in the transparent administration of over 2 billion vaccine doses.

- Labour markets have recovered beyond pre-Covid levels, in both urban and rural areas, with unemployment rates falling from 5.8 per cent in 2018-19 to 4.2 per cent in 2020-21.

- The year FY22 saw improvement in Gross Enrolment Ratios (GER) in schools and improvement in gender parity. GER in the primary-enrolment in class I to V as a percentage of the population in age 6 to 10 years - for girls as well as boys have improved in FY22.

- Due to several steps taken by the government on health, out-of-pocket expenditure as a percentage of total health expenditure declined from 64.2% in FY14 to 48.2% in FY19.

- Infant Mortality Rate (IMR), Under Five mortality rate (U5MR) and neonatal Mortality Rate (NMR) have shown a steady decline.

- More than 220 crore COVID vaccine doses administered as on 06 January, 2023.

- Nearly 22 crore beneficiaries have been verified under the Ayushman Bharat Scheme as on 04 January, 2023. Over 1.54 lakh Health and Wellness Centres have been operationalized across the country under Ayushman Bharat.

Climate Change and Environment: Preparing to Face the Future

- India declared the Net Zero Pledge to achieve net zero emissions goal by 2070.

- India achieved its target of 40 per cent installed electric capacity from non-fossil fuels ahead of 2030.

- The likely installed capacity from non-fossil fuels to be more than 500 GW by 2030 resulting in decline of average emission rate by around 29% by 2029-30, compared to 2014-15.

- India to reduce emissions intensity of its GDP by 45% by 2030 from 2005 levels.

- About 50% cumulative electric power installed capacity to come from non-fossil fuel-based energy resources by 2030.

- A mass movement LIFE– Life style for Environment launched.

- Sovereign Green Bond Framework (SGrBs) issued in November 2022.

- RBI auctions two tranches of ₹4,000 crore Sovereign Green Bonds (SGrB).

- National Green Hydrogen Mission to enable India to be energy independent by 2047.

- Green hydrogen production capacity of at least 5 MMT (Million Metric Tonne) per annum to be developed by 2030. Cumulative reduction in fossil fuel imports over ₹1 lakh crore and creation of over 6 lakh jobs by 2030 under the National green Hydrogen Mission. Renewable energy capacity addition of about 125 GW and abatement of nearly 50 MMT of annual GHG emissions by 2030.

- The Survey highlights the progress on eight missions under the NAP on CC to address climate concerns and promote sustainable development.

- Solar power capacity installed, a key metric under the National Solar Mission stood at 61.6 GW as on October 2022.

- India becoming a favored destination for renewables; investments in 7 years stand at USD 78.1 billion.

- 62.8 lakh individual household toilets and 6.2 lakh community and public toilets constructed (August 2022) under the National Mission on Sustainable Habitat.

Agriculture and Food Management

- The performance of the agriculture and allied sector has been buoyant over the past several years, much of which is on account of the measures taken by the government to augment crop and livestock productivity, ensure certainty of returns to the farmers through price support, promote crop diversification, improve market infrastructure through the impetus provided for the setting up of farmer-producer organisations and promotion of investment in infrastructure facilities through the Agriculture Infrastructure Fund.

- Private investment in agriculture increases to 9.3% in 2020-21.

- MSP for all mandated crops fixed at 1.5 times of all India weighted average cost of production since 2018.

- Institutional Credit to the Agricultural Sector continued to grow to 18.6 lakh crore in 2021-22

- Foodgrains production in India saw sustained increase and stood at 315.7 million tonnes in 2021-22.

- Free foodgrains to about 81.4 crore beneficiaries under the National Food Security Act for one year from January 1, 2023.

- About 11.3 crore farmers were covered under the Scheme in its April-July 2022-23 payment cycle.

- Rs 13,681 crores sanctioned for Post-Harvest Support and Community Farms under the Agriculture Infrastructure Fund.

- Online, Competitive, Transparent Bidding System with 1.74 crore farmers and 2.39 lakh traders put in place under the National Agriculture Market (e-NAM) Scheme.

- Organic Farming being promoted through Farmer Producer Organisations (FPO) under the Paramparagat Krishi Vikas Yojana (PKVY).

- India stands at the forefront to promote millets through the International Year of Millets initiative.

Industry: Steady Recovery

- Overall Gross Value Added (GVA) by the Industrial Sector (for the first half of FY 22-23) rose 3.7 per cent, which is higher than the average growth of 2.8 per cent achieved in the first half of the last decade.

- Robust growth in Private Final Consumption Expenditure, export stimulus during the first half of the year, increase in investment demand triggered by enhanced public capex and strengthened bank and corporate balance sheets have provided a demand stimulus to industrial growth.

- The supply response of the industry to the demand stimulus has been robust.

- PMI manufacturing has remained in the expansion zone for 18 months since July 2021, and Index of Industrial Production (IIP) grows at a healthy pace.

- Credit to Micro, Small and Medium Enterprises (MSMEs) has grown by an average of around 30% since January 2022 and credit to large industry has been showing double-digit growth since October 2022.

- Electronics exports rise nearly threefold, from US $4.4 billion in FY19 to US $11.6 Billion in FY22.

- India has become the second-largest mobile phone manufacturer globally, with the production of handsets going up from 6 crore units in FY15 to 29 crore units in FY21.

- Foreign Direct Investment (FDI) flows into the Pharma Industry has risen four times, from US $180 million in FY19 to US $699 million in FY22.

- The Production Linked Incentive (PLI) schemes introduced across 14 categories, with an estimated capex of ₹4 lakh crore over the next five years, to plug India into global supply chains. Investment of ₹47,500 crores has been seen under the PLI schemes in the FY22, which is 106% of the designated target for the year. Production/sales worth ₹3.85 lakh crore and employment generation of 3.0 lakh have been recorded due to PLI schemes.

- Over 39,000 compliances have been reduced and more than 3500 provisions decriminalized as of January 2023.

Services: Source of Strength

- The services sector is expected to grow at 9.1% in FY23, as against 8.4% (YoY) in FY22.

- Robust expansion in PMI services, indicative of service sector activity, observed since July 2022.

- India was among the top ten services exporting countries in 2021, with its share in world commercial services exports increasing from 3 per cent in 2015 to 4 per cent in 2021.

- India’s services exports remained resilient during the Covid-19 pandemic and amid geopolitical uncertainties driven by higher demand for digital support, cloud services, and infrastructure modernization.

- Credit to services sector has grown by over 16% since July 2022.

- US$ 7.1 billion FDI equity inflows in services sector in FY22.

- Contact-intensive services are set to reclaim pre-pandemic level growth rates in FY23.

- Sustained growth in the real estate sector is taking housing sales to pre-pandemic levels, with a 50% rise between 2021 and 2022.

- Hotel occupancy rate has improved from 30-32% in April 2021 to 68-70% in November 2022.

- Tourism sector is showing signs of revival, with foreign tourist arrivals in India in FY23 growing month-on-month with resumption of scheduled international flights and easing of Covid-19 regulations.

- Digital platforms are transforming India’s financial services.

- India’s e-commerce market is projected to grow at 18 per cent annually through 2025.

External Sector

- Merchandise exports were US$ 332.8 billion for April-December 2022.

- India diversified its markets and increased its exports to Brazil, South Africa and Saudi Arabia.

- To increase its market size and ensure better penetration, in 2022, CEPA with UAE and ECTA with Australia come into force.

- India is the largest recipient of remittances in the world receiving US$ 100 bn in 2022. Remittances are the second largest major source of external financing after service export

- As of December 2022, Forex Reserves stood at US$ 563 bn covering 9.3 months of imports.

- As of end-November 2022, India is the sixth largest foreign exchange reserves holder in the world.

- The current stock of external debt is well shielded by the comfortable level of foreign exchange reserves.

- India has relatively low levels of total debt as a percentage of Gross National Income and short-term debt as a percentage of total debt.

Physical and Digital Infrastructure

Government’s Vision for Infrastructure Development

- Public Private Partnerships

- In-Principal Approval granted to 56 projects with Total Project Cost of ₹57,870.1 crore under the VGF Scheme, from 2014-15 to 2022-23.

- IIPDF Scheme with ₹150 crore outlay from FY 23-25 was notified by the government on 03 November, 2022.

- National Infrastructure Pipeline

- 89,151 projects costing ₹141.4 lakh crore under different stages of implementation

- 1009 projects worth ₹5.5 lakh crore completed

- NIP and Project Monitoring Group (PMG) portal linkage to fast-track approvals/ clearances for projects

- National Monetisation Pipeline

- ₹ 9.0 lakh crore is the estimated cumulative investment potential.

- ₹ 0.9 lakh crore monetisation target achieved against expected ₹0.8 lakh crore in FY22.

- FY23 target is envisaged to be ₹1.6 lakh crore (27 per cent of overall NMP Target)

- GatiShakti

- PM GatiShakti National Master Plan creates comprehensive database for integrated planning and synchronised implementation across Ministries/ Departments.

- Aims to improve multimodal connectivity and logistics efficiency while addressing the critical gaps for the seamless movement of people and goods.

Electricity Sector and Renewables

- As on 30 September 2022, the government has sanctioned the entire target capacity of 40 GW for the development of 59 Solar Parks in 16 states.

- 17.2 lakh GWh electricity generated during the year FY22 compared to 15.9 lakh GWh during FY21.

- The total installed power capacity (industries having demand of 1 Mega Watt (MW) and above) increased from 460.7 GW on 31 March 2021 to 482.2 GW on 31 March 2022.

Making Indian Logistics Globally Competitive

- National Logistics Policy envisions to develop a technologically enabled, integrated, cost-efficient, resilient, sustainable and trusted logistics ecosystem in the country for accelerated and inclusive growth.

- Rapid increase in National Highways (NHs) /Roads Construction with 10457 km NHs/roads constructed in FY22 compared to 6061 km in FY16.

- Budget expenditure increased from ₹1.4 lakh crore in FY20 to ₹2.4 lakh crore in FY23 giving renewed push to Capital expenditure.

- 2359 Kisan rails transported approximately 7.91 lakh tonnes of perishables, as of October 2022.

- More than one crore air passengers availed the benefit of the UDAN scheme since its inception in 2016.

- Near doubling of capacity of major ports in 8 years.

- Inland Vessels Act 2021 replaced 100-year-old Act to ensure hassle free movement of Vessels promoting Inland Water Transport.

India’s Digital Public Infrastructure

- Unified Payment Interface (UPI)

- UPI-based transactions grew in value (121 per cent) and volume (115 per cent) terms, between 2019-22, paving the way for its international adoption.

- Telephone and Radio - For Digital Empowerment

- Total telephone subscriber base in India stands at 117.8 crore (as of Sept,22), with 44.3 per cent of subscribers in rural India.

- More than 98 per cent of the total telephone subscribers are connected wirelessly.

- The overall tele-density in India stood at 84.8 per cent in March 22.

- 200 per cent increase in rural internet subscriptions between 2015 and 2021.

- Prasar Bharati (India’s autonomous public service broadcaster) - broadcasts in 23 languages, 179 dialects from 479 stations. Reaches 92 per cent of the area and 99.1 per cent of the total population.

- Digital Public Goods

- Achieved low-cost accessibility since the launch of Aadhaar in 2009

- Under the government schemes, MyScheme, TrEDS, GEM, e-NAM, UMANG has transformed market place and has enabled citizens to access services across sectors

- Under Account Aggregator, the consent-based data sharing framework is currently live across over 110 crore bank accounts.

- Open Credit Enablement Network aims towards democratising lending operations while allowing end-to-end digital loan applications

- National AI portal has published 1520 articles, 262 videos, and 120 government initiatives and is being viewed as viewed as a tool for overcoming the language barrier e.g. ‘Bhashini’.

- Legislations are being introduced for enhanced user privacy and creating an ecosystem for standard, open, and interoperable protocols underlining robust data governance.

***

RM/AD/VD/DJM/LP/RC/SSV

(Release ID: 1894929)

Ministry of Finance

MAJOR ANNOUNCEMENTS IN PERSONAL INCOME TAX TO SUBSTANTIALLY BENEFIT THE MIDDLE CLASS

PERSONS WITH INCOME UP TO RS. 7 LAKH WILL NOT PAY INCOME TAX IN NEW TAX REGIME

TAX EXEMPTION LIMIT INCREASED TO RS. 3 LAKH

CHANGE IN TAX STRUCTURE: NUMBER OF SLABS REDUCED TO FIVE

SALARIED CLASS AND PENSIONERS TO GAIN ON EXTENSION OF STANDARD DEDUCTION BENEFIT TO THE NEW TAX REGIME

MAXIMUM TAX RATE REDUCED TO 39 PER CENT FROM 42.74 PER CENT

NEW TAX REGIME TO BE THE DEFAULT TAX REGIME

CITIZENS TO HAVE THE OPTION TO AVAIL THE BENEFIT OF OLD TAX REGIME

Dated: 01 FEB 2023

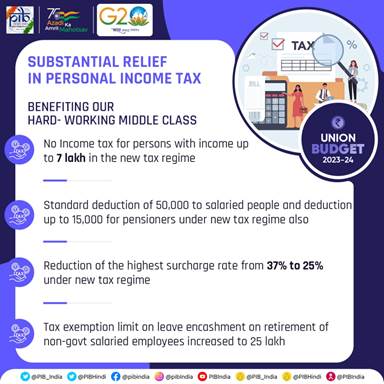

With the objective of benefitting the hard working middle class of the country, Union Minister for Finance and Corporate Affairs, Smt. Nirmala Sitaraman made five major announcements with respect to personal income tax while presenting the Union Budget 2023-24 in Parliament today. These announcements pertaining to rebate, change in tax structure, extension of benefit of standard deduction to the new tax regime, reduction of highest surcharge rate and extension of limit of tax exemption on leave encashment on retirement of non-government salaried employees will provide substantial benefits to the working middle class.

In her first announcement regarding rebate, she proposed to increase the rebate limit to Rs.7 lakh in the new tax regime, which would mean that the persons in the new tax regime, with income up to Rs. 7 lakh will not have to pay any tax. Currently, those with income up to Rs. 5 lakh do not pay any income tax in both old and new tax regimes.

Providing relief to middle-class individuals, she proposed a change in the tax structure in the new personal income tax regime by reducing the number of slabs to five and increasing the tax exemption limit to Rs. 3 lakh. The new tax rates are:

|

Total income (Rs.) |

Rate (per cent) |

|

Upto 0-3 lakh |

Nil |

|

From 3-6 lakh |

5 |

|

From 6-9 lakh |

10 |

|

From 9-12 lakh |

15 |

|

From 12-15 lakh |

20 |

|

Above 15 lakh |

30 |

This will provide major relief to all tax payers in the new regime. An individual with an annual income of Rs. 9 lakh will be required to pay only Rs. 45,000/-. This is only 5 per cent of his or her income. It is a reduction of 25 per cent on what he or she is required to pay now, i.e. Rs. 60,000/-. Similarly, an individual with an income of Rs. 15 lakh would be required to pay only Rs. 1.5 lakh or 10 per cent of his or her income, a reduction of 20 per cent from the existing liability of Rs. 1,87,500/.

The third proposal of the budget provides major relief to the salaried class and the pensioners including family pensioners as the Finance Minister proposed to extend the benefit of standard deduction to the new tax regime. Each salaried person with an income of Rs. 15.5 lakh or more will thus stand to benefit by Rs. 52,500/-. At present, standard deduction of Rs. 50,000/- to salaried individuals and deduction from family pension up to Rs. 15,000/- is currently allowed only under the old regime.

As part of her fourth announcement with respect to personal income tax, Smt. Nirmala Sitaraman proposed to reduce the highest surcharge rate from 37 per cent to 25 per cent in the new tax regime for income above Rs. 2 crore. This would result in reduction of the maximum tax rate to 39 per cent from the present 42.74 per cent, which is among the highest in the world. However, no change in surcharge is proposed for those who opt to be under the old regime in this income group.

As part of the fifth announcement, the budget proposed extension of limit of tax exemption on leave encashment to Rs. 25 lakh on retirement of non-government salaried employees in line with the government salaried class. At present, the maximum amount which can be exempted is Rs. 3 lakh.

The budget proposed to make the new income tax regime as the default tax regime. However, citizens will continue to have the option to avail the benefit of the old tax regime.

******

RM/PPG/RC

(Release ID: 1895286)

DIRECT TAXES

Direct Tax proposals aim to maintain continuity and stability of taxation, further simplify and rationalise various provisions to reduce the compliance burden, promote the entrepreneurial spirit and provide tax relief to citizens.

Constant endeavour of the Income Tax Department to improve Tax Payers Services by making compliance easy and smooth.

To further improve tax payer services, proposal to roll out a next-generation Common IT Return Form for tax payer convenience, along with plans to strengthen the grievance redressal mechanism.

Rebate limit of Personal Income Tax to be increased to Rs. 7 lakh from the current Rs. 5 lakh in the new tax regime. Thus, persons in the new tax regime, with income up to Rs. 7 lakh to not pay any tax.

Tax structure in new personal income tax regime, introduced in 2020 with six income slabs, to change by reducing the number of slabs to five and increasing the tax exemption limit to Rs. 3 lakh. Change to provide major relief to all tax payers in the new regime.

New tax rates

|

Total Income (Rs) |

Rate (per cent) |

|

Up to 3,00,000 |

Nil |

|

From 3,00,001 to 6,00,000 |

5 |

|

From 6,00,001 to 9,00,000 |

10 |

|

From 9,00,001 to 12,00,000 |

15 |

|

From 12,00,001 to 15,00,000 |

20 |

|

Above 15,00,000 |

30 |

Proposal to extend the benefit of standard deduction of Rs. 50,000 to salaried individual, and deduction from family pension up to Rs. 15,000, in the new tax regime.

Highest surcharge rate to reduce from 37 per cent to 25 per cent in the new tax regime. This to further result in reduction of the maximum personal income tax rate to 39 per cent.

The limit for tax exemption on leave encashment on retirement of non-government salaried employees to increase to Rs. 25 lakh.

The new income tax regime to be made the default tax regime. However, citizens will continue to have the option to avail the benefit of the old tax regime.

Enhanced limits for micro enterprises and certain professionals for availing the benefit of presumptive taxation proposed. Increased limit to apply only in case the amount or aggregate of the amounts received during the year, in cash, does not exceed five per cent of the total gross receipts/turnover.

Deduction for expenditure incurred on payments made to MSMEs to be allowed only when payment is actually made in order to support MSMEs in timely receipt of payments.

New co-operatives that commence manufacturing activities till 31.3.2024 to get the benefit of a lower tax rate of 15 per cent, as presently available to new manufacturing companies.

Opportunity provided to sugar co-operatives to claim payments made to sugarcane farmers for the period prior to assessment year 2016-17 as expenditure. This expected to provide them a relief of almost Rs. 10,000 crore.

Provision of a higher limit of Rs. 2 lakh per member for cash deposits to and loans in cash by Primary Agricultural Co-operative Societies (PACS) and Primary Co-operative Agriculture and Rural Development Banks (PCARDBs).

A higher limit of Rs. 3 crore for TDS on cash withdrawal to be provided to co-operative societies.

Date of incorporation for income tax benefits to start-ups to be extended from 31.03.23 to 31.3.24.

Proposal to provide the benefit of carry forward of losses on change of shareholding of start-ups from seven years of incorporation to ten years.

Deduction from capital gains on investment in residential house under sections 54 and 54F to be capped at Rs. 10 crore for better targeting of tax concessions and exemptions.

Proposal to limit income tax exemption from proceeds of insurance policies with very high value. Where aggregate of premium for life insurance policies (other than ULIP) issued on or after 1st April, 2023 is above Rs. 5 lakh, income from only those policies with aggregate premium up to Rs. 5 lakh shall be exempt.

Income of authorities, boards and commissions set up by statutes of the Union or State for the purpose of housing, development of cities, towns and villages, and regulating, or regulating and developing an activity or matter, proposed to be exempted from income tax.

Minimum threshold of Rs. 10,000/- for TDS to be removed and taxability relating to online gaming to be clarified. Proposal to provide for TDS and taxability on net winnings at the time of withdrawal or at the end of the financial year.

Conversion of gold into electronic gold receipt and vice versa not to be treated as capital gain.

TDS rate to be reduced from 30 per cent to 20 per cent on taxable portion of EPF withdrawal in non-PAN cases.

Income from Market Linked Debentures to be taxed.

Deployment of about 100 Joint Commissioners for disposal of small appeals in order to reduce the pendency of appeals at Commissioner level.

Increased selectivity in taking up appeal cases for scrutiny of returns already received this year.

Period of tax benefits to funds relocating to IFSC, GIFT City extended till 31.03.2025.

Certain acts of omission of liquidators under section 276A of the Income Tax Act to be decriminalized with effect from 1st April, 2023.

Carry forward of losses on strategic disinvestment including that of IDBI Bank to be allowed.

Agniveer Fund to be provided EEE status. The payment received from the Agniveer Corpus Fund by the Agniveers enrolled in Agnipath Scheme, 2022 proposed to be exempt from taxes. Deduction in the computation of total income is proposed to be allowed to the Agniveer on the contribution made by him or the Central Government to his Seva Nidhi account.

Government of India

Ministry of Finance

Department of Revenue

Central Board of Direct Taxes

******

New Delhi, 11th January, 2023

PRESS RELEASE

Direct Tax Collections for F.Y. 2022-23 up to 10.01.2023

The provisional figures of Direct Tax collections up to 10th January, 2023 continue to register steady growth. Direct Tax collections up to 10th January, 2023 show that gross collections are at Rs. 14.71 lakh crore which is 24.58% higher than the gross collections for the corresponding period of last year. Direct Tax collection, net of refunds, stands at Rs. 12.31 lakh crore which is 19.55 % higher than the net collections for the corresponding period of last year. This collection is 86.68% of the total Budget Estimates of Direct Taxes for F.Y. 2022-23.

So far as the growth rate for Corporate Income Tax (CIT) and Personal Income Tax (PIT) in terms of gross revenue collections is concerned, the growth rate for CIT is 19.72% while that for PIT (including STT) is 30.46%. After adjustment of refunds, the net growth in CIT collections is 18.33% and that in PIT collections is 21.64% (PIT only)/ 20.97% (PIT including STT).

Refunds amounting to Rs.2.40 lakh crore have been issued during 1st April, 2022 to 10th January 2023, which are 58.74% higher than refunds issued during the same period in the preceding year.

(Surabhi Ahluwalia)

Pr. Commissioner of Income Tax

(Media & Technical Policy)

Official Spokesperson, CBDT.

Government of India

Ministry of Finance

Department of Revenue

Central Board of Direct Taxes

New Delhi, 18th December, 2022

PRESS RELEASE

Gross Direct Tax collections for the Financial Year (FY) 2022-23 register a growth of 25.90%

Net Direct Tax collections for the FY 2022-23have grown at over 19.81%

Advance Tax collections for the FY 2022-23 stand at Rs. 5,21,302 crore as on 17.12.2022 which shows a growth of 12.83%

Refunds aggregating to Rs. 2,27,896 crore have been issued in the current fiscal

The figures of Direct Tax collections for the Financial Year 2022-23, as on 17.12.2022 show that net collections are at Rs. 11,35,754 crore, compared to Rs. 9,47,959 crore in the corresponding period of the preceding Financial Year i.e FY 2021-22, representing an increase of 19.81%.

The Net Direct Tax collection of Rs. 11,35,754 crore (as on 17.12.2022) includes Corporation Tax (CIT) at Rs. 6,06,679 crore (net of refund) and Personal Income Tax (PIT) including Securities Transaction Tax(STT) at Rs. 5,26,477 crore (net of refund).

The Gross collection of Direct Taxes (before adjusting for refunds) for the FY 2022-23 stands at Rs. 13,63,649 crore compared to Rs. 10,83,150 crore in the corresponding period of the preceding financial year, registering a growth of 25.90% over collections of F.Y. 2021-22.

The Gross collection of Rs. 13,63,649 crore includes Corporation Tax (CIT) at Rs. 7,25,036 crore and Personal Income Tax (PIT) including Securities Transaction Tax(STT) at Rs. 6,35,920 crore. Minor head wise collection comprises Advance Tax of Rs. 5,21,302 crore; Tax Deducted at Source of Rs. 6,44,761 crore; Self-Assessment Tax of Rs. 1,40,105 crore; Regular Assessment Tax of Rs. 46,244 crore; and Tax under other minor heads of Rs. 11,237 crore.

The cumulative Advance Tax collections for the first, second and third quarter of the F.Y. 2022-23 stand at Rs. 5,21,302 crore as on 17.12.2022, against Advance Tax collections of Rs. 4,62,038 crore for the corresponding period of the immediately preceding Financial Year i.e. 2021-22, showing a growth of 12.83%. The Advance Tax collection of Rs. 5,21,302 crore as on 17.12.2022 includes Corporation Tax (CIT) at Rs. 3,97,364 crore and Personal Income Tax (PIT) at Rs. 1,23,936 crore.

There has been a remarkable increase in the speed of processing of income tax returns filed during the current fiscal, with almost 96.5% of the duly verified ITRs having been processed till 17.12.2022. This has resulted in faster issue of refunds with almost a 109% increase in the number of refunds issued in the current financial year. Refunds amounting to Rs. 2,27,896 crore have been issued in the FY 2022-23 till 17.12.2022, as against refunds of Rs.1,35,191 crore issued during the corresponding period in the preceding Financial Year 2021-22, showing a growth of over 68.57%.

(Surabhi Ahluwalia)

Pr. Commissioner of Income Tax

(Media & Technical Policy)

Official Spokesperson, CBDT