The Department of Financial Services (DFS) continued its momentum of reforms in 2024, building on the robust foundation established through initiatives like the EASE Reform agenda, which emphasises risk assessment, NPA management, financial inclusion, customer service, digital transformation, and more.

The EASE Reforms, governed by the EASE Steering Committee of the Indian Bank's Association, are now a well-established framework in all Public Sector Banks (PSBs). From EASE 1.0 to the current EASE 7.0, the reforms have brought a transformative shift, focusing on digital customer experience, analytics-driven business strategies, technology-enabled capability building, and enhanced HR operations. The annual EASE Awards event continues to recognise exceptional performances in implementing the reform agenda.

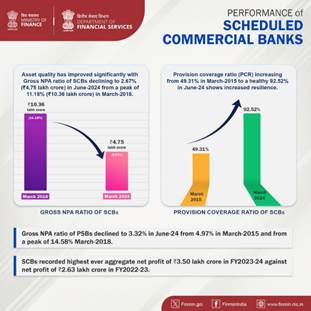

DFS’s strategic interventions have significantly contributed to the reduction of Non-Performing Assets (NPAs) in Scheduled Commercial Banks (SCBs). Gross NPAs have decreased from Rs. 10.36 lakh crore in March 2018 to Rs. 4. 75 lakh crore in March 2024, reflecting the efficacy of measures such as the Insolvency and Bankruptcy Code (IBC), amendments to the SARFAESI Act, and the Prudential Framework for Resolution of Stressed Assets.

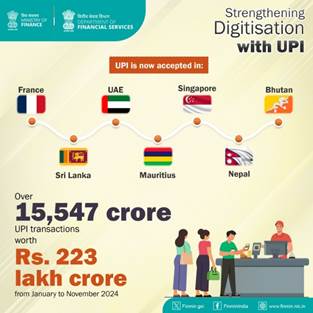

In digital payments, the DFS has strengthened its leadership role, driving consistent growth through the DIGIDHAN Mission. Digital payment transactions surged further to an unprecedented 223 lakh crore from January to November 2024, with BHIM-UPI recording over 15,547 crore transactions during the same period, underscoring its role as a key enabler of India’s digital economy.

Financial inclusion remains a top priority, with initiatives like the Pradhan Mantri Jan Dhan Yojana (PMJDY), Pradhan Mantri Jeevan Jyoti Bima Yojana, Pradhan Mantri Suraksha Bima Yojana, MUDRA, Stand Up India, and Atal Pension Yojana making significant progress. As of 2024, these schemes have expanded their reach, ensuring that millions of citizens, especially from marginalized communities, gain access to essential banking, insurance, and pension services.

In the agriculture sector, the DFS has facilitated record credit disbursements, with Agricultural Credit increasing from Rs. 8.45 lakh crore in FY 2014-15 to Rs. 24.30 lakh crore in FY 2023-24. The Kisan Credit Card (KCC) scheme continues to play a pivotal role, with over 7.92 crore active KCC accounts, providing farmers with timely and hassle-free credit support.

The Department of Financial Services has been instrumental in shaping a resilient and progressive financial landscape in 2024, contributing significantly to India’s economic growth and social well-being.

Following are some of the major achievements & policy initiatives of the Department of Financial Services, Ministry of Finance, in 2024:

PERFORMANCE OF BANKS

As a result of Government’s overarching policy response to recognition of stress, resolution of stressed accounts, recapitalisation and reforms in banks, the financial health and robustness of banking sector has since improved significantly.

- As per RBI’s provisional data:

- Asset quality has improved significantly with—

- Gross NPA ratio of SCBs declining to 2.67% (₹4.75 lakh crore) in Jun-24 from 4.28% (₹3.23 lakh crore) in Mar-15 and from a peak of 11.18% (₹10.36 lakh crore) in Mar-18.

- Gross NPA ratio of PSBs declining to 3.32% (₹3.29 lakh crore) in Jun-24 from 4.97% (₹2.79 lakh crore) in Mar-15 and from a peak of 14.58% (₹8.96 lakh crore) Mar-18.

- Net NPAs of SCBs declining to ₹1.05 lakh crore (0.6%) in Jun-24 from ₹2.31 lakh crore (3.13%) in Mar-15 and from a peak of ₹5.2 lakh crore (5.94%) in Mar-18.

- Net NPAs of PSBs declining to ₹0.68 lakh crore (0.71%) in Jun-24 from ₹2.15 lakh crore (3.92%) in Mar-15 and from a peak of ₹4.54 lakh crore (7.97%) in Mar-18.

- Resilience has increased with—

- Provision coverage ratio (PCR) of SCBs increasing from 49.31% in Mar-15 to a healthy 92.52% in Jun-24.

- PCR of PSBs increasing from 46.04% in Mar-15 to a healthy 93.36% in Jun-24.

- Capital adequacy has improved significantly with—

- CRAR of SCBs improving by 185 bps to reach 14.79% in Jun-24 from 12.94% in Mar-15.

- CRAR of PSBs improving by 173 bps to reach 13.18% in Jun-24 from 11.45% in Mar-15.

- During FY2023-24, SCBs have recorded highest ever aggregate net profit of ₹3.50 lakh crore against net profit of ₹2.63 lakh crore in FY2022-23.

In FY2023-24, PSBs have recorded highest ever aggregate net profit of ₹1.41 lakh crore against net profit of ₹1.05 lakh crore in FY2022-23, and recorded ₹0.40 lakh crore in the first quarter of FY2024-25.

- PSBs declared dividend of ₹27,830 crore to shareholders (GoI share ₹18,013 crore) in FY2023-24 against total dividend of ₹20,964 crore to shareholders (GoI share ₹13,804) in FY2022-23.

- Enabled by implementation of comprehensive reforms, the financial health of PSBs has improved significantly, enhancing their ability to raise capital (in the form of both equity and bonds) from the market. PSBs have mobilised capital of ₹4.34 lakh crore from the market from FY2014-15 to FY2023-24.

- Banks, earlier placed under Prompt Corrective Action (PCA) framework by RBI, have made significant improvement resulting in removal of each one of them from the PCA restrictions.

By addressing issues of NPAs and recapitalisation, the reforms contributed to improve the overall credit flow in the economy. PSBs emerged healthier and are poised to facilitate growth in productive sectors of the economy.

DIGITAL PAYMENTS

- Google Pay India signs Memorandum of Understanding (MoU) with National Payments Corporation of India (NPCI) International for Global Expansion of Unified Payments Interface (UPI).

- UPI is now accepted in France.

- BOBCARD Limited launches Corporate Credit Card on RuPay Network.

- NPCI International and Eurobank Sign MoU in view of forming a strategic alliance on Foreign Inward Remittances (FIR).

- UPI is now accepted in Nepal.

- NPCI Bharat BillPay partners with State Bank of India (SBI) to introduce National Common Mobility Card (NCMC) recharge as a new biller category.

- RuPay Unveils 'Link it, Forget it' campaign at Indian Premium League (IPL) 2024 to promote RuPay Credit Card on UPI.

- NPCI International partners with Bank of Namibia for deploying India’s UPI Stack in Namibia.

- RuPay Credit & Debit Cardholders can now avail 25% cashback on in-store purchases in Canada, Japan, Spain, Switzerland, United Arab Emirates (UAE), United Kingdom (UK), and United States of America (USA).

- NPCI International and the Central Reserve Bank of Peru Partner to develop UPI like real time payments system in Peru.

- NPCI International partners with Network International to enable UPI QR (Quick Response) payment acceptance across its merchants in the UAE.

- NPCI International partners with Qatar National Bank (QNB) to launch UPI Payments in Qatar.

- “UPI One World” wallet service extends to all* inbound international travellers.

- UPI merchant transactions in Nepal surpass 100,000 mark.

Key Digital Payment Initiatives at Global Fintech Festival 2024:

- Bharat BillPay for Business (Business to Business (B2B) Platforms): The Reserve Bank of India (RBI) Governor announced the expansion of Bharat Bill Payment System (BBPS) services to cater to business enablement platforms, streamlining B2B payments and collections. This development is expected to change the landscape of business payments across the country through a single, centralized, interoperable platform.

- UPI Circle (Delegate Payments): UPI Circle is a feature enabling UPI user to act as a primary user linking with trusted secondary users on UPI app for either partial or full delegation of payments. In full delegation, the primary user authorizes a trusted secondary user to initiate and complete UPI transactions as per defined spend limits.

- Bharat Interface for Money (BHIM) to Empower Artisans under PM Vishwakarma Scheme through e-RUPI Vouchers.

- NPCI International to develop UPI-like Real-Time Payments Platform in Trinidad and Tobago.

UPI:

- UPI Lite was brought within ambit of the e-mandate framework by introducing an auto-replenishment facility for loading the UPI Lite wallet by the customer, if the balance goes below a threshold amount set by him/her.

- UPI limits for tax payments increased from ₹1 lakh to ₹5 lakh per transaction.

- Introduced "Delegated Payments" in UPI which allows an individual (primary user) to set a UPI transaction limit for another individual (secondary user) on the primary user’s bank account.

- Per-transaction limit in UPI123Pay has been increased to ₹10,000 to widen the use-cases.

- UPI Lite: The overall limit of UPI Lite has been increased to ₹5,000 with a per-transaction limit to ₹1,000.

Prepaid Payment Instruments (PPIs):

- To promote use of digital payments for various public transport systems and transit purposes, including NCMC cards and FASTags, the guidelines on prepaid payment instruments have been amended by dispensing with the KYC criteria for PPI - mass transit systems. This is expected to boost issuance of such instruments which have specific end-use, providing greater convenience and speed to the customers.

Internet Banking:

- A payment system for internet banking for online merchant payment transactions was announced. This will bring the benefits of interoperability to ecosystem and quicker settlement for merchants; especially benefiting segments such as collection of tax, insurance premium, mutual fund payments, etc.

Bharat Bill Payment System (BBPS) Issuance of Master Direction:

- BBPS is a payment system operated by NPCI Bharat Bill Pay Limited (NBBL), a NPCI subsidiary, which facilitates payment and settlement of utility bills, FASTag recharge, Credit Card bill payments, payments to educational institutes, etc. NBBL is the central unit while banks and authorised non-bank Payment Service Providers (PSPs) act as Bharat Bill Payment Operating Units (BBPOUs). BBPOUs can be of two types – (i) Biller Operating Units (BOUs) who onboard billers and, (ii) Customer Operating Units (COUs) who give access to customers. BBPS guidelines were first issued in November 2014. In view of the subsequent developments in the payments ecosystem, the need to review the above guidelines had arisen. “Master Direction – Reserve Bank of India (Bharat Bill Payment System) Directions, 2024” was issued by the RBI on February 29, 2024.

- The major changes include (i) expanding the participation criteria to all authorised non-bank Payment Aggregators, (ii) measures to enhance interoperability, (iii) customer protection measures and (iv) requirement of Escrow account for non-bank BBPOUs to ensure protection of funds from insolvency.

Card-based Payments:

- To promote cardholder with a choice of network, Reserve Bank of India has issued instructions which refrain card issuers from entering any arrangement that restrain them from availing services of other card networks. Further, in case of credit cards issuance, card issuers shall provide an option to their eligible customers to choose from amongst multiple card networks.

Accessibility to Payment Systems for Persons with Disabilities:

- All sections of population, including differently abled persons, are increasingly adopting digital payment systems. To promote effective access, payment system participants (PSPs, that is, banks and authorised non-bank payment system providers) were advised to review their payment systems / devices in terms of accessibility to Persons with Disabilities.

Digitally Enabled Market Cluster:

- As announced by Governor, Reserve Bank of India, during the Digital Payments Awareness Week (DPAW) 2024 observed during March 04-10, 2024, Regional offices (ROs) of the Reserve Bank have started campaigns to identify and develop marketplaces like vegetable markets / mandis and public transport infrastructure like auto/ taxi drivers as digitally enabled clusters in their chosen areas. Identified market clusters shall be considered as digitally enabled if at least 80% of the market cluster has digital payment acceptance infrastructure.

Introduction of beneficiary account name look-up facility:

- Introduction of beneficiary account name look-up facility was announced in Statement on Developmental and Regulatory Policies on October 09, 2024 by Governor. Payment Systems like UPI and IMPS provide a facility to the remitter to verify the name of the receiver (beneficiary) before initiating a payment transaction. There have been requests to introduce such a facility for Real Time Gross Settlement System (RTGS) and National Electronic Funds Transfer (NEFT) systems.

- Accordingly, to enable remitters in RTGS and NEFT to verify the name of the beneficiary account before initiating funds transfer, a ‘beneficiary account name look-up facility’ will be introduced. Remitters can input the account number and the Indian Financial System Code (IFSC) of the beneficiary, following which the name of the beneficiary will be displayed. This facility will increase customer confidence as it would reduce the possibility of wrong credits and frauds.

Internationalisation Initiatives

- In 2024, acceptance of India’s UPI apps via QR Code has been operationalised in France, Sri Lanka, Mauritius, and Nepal. In case of Mauritius, the arrangement enables Mauritian Fast Payment System apps to scan UPI QR Codes in India as well.

- Mauritius has become the first country outside Asia to issue cards using RuPay technology. With the adoption of RuPay technology, the Mauritius Central Automated Switch (MauCAS) card scheme will enable banks in Mauritius to issue RuPay cards domestically. Such cards can be used at ATMs and PoS terminals locally in Mauritius as well as in India.

UPI achievements during last 3 years:

|

2021-2022 |

|

|

2022-2023 |

|

|

2023-2034 |

|

Staff Welfare Fund

Staff welfare fund (SWF) is a fund allocated by the PSBs for the welfare-related activities (health-related expenses, subsidies on canteen, sports and cultural activities, education-related financial assistance etc.) in respect of working and retired officials of PSBs. SWF was given a fillip by increasing the maximum ceiling of annual spending. The ceiling, last revised in 2012, was thoroughly revised after taking into consideration the number of employees and retirees in PSBs as of 2024 and the change in the business mix of the PSBs. PSBs were categorized into four different slabs based on their business mix and the employee strength and the ceilings were revised accordingly. Post revision, the combined maximum annual expenditure ceiling of SWF for all the 12 PSBs has increased from Rs.540 crore to Rs.845 crore. This increase will benefit 15 lakh staff including the retired employees of all the 12 PSBs.

Creation / Increase of Chief General Manager Posts In Nationalised Banks

Union Finance Minister has approved the creation of Chief General Manager (CGM) posts in five additional nationalized banks: Bank of Maharashtra, Central Bank of India, Indian Overseas Bank, Punjab & Sind Bank, and UCO Bank. Previously, CGM posts existed in only six out of eleven nationalized banks. This decision will increase the number of CGM posts, enhancing the administrative and functional structure within the banks. CGM posts serve as a critical link between General Managers (GMs) and Executive Directors, improving oversight and supervision in areas like digitalization, cybersecurity, and financial inclusion.

The number of CGM posts will now be based on a ratio of one CGM for every four GMs. This expansion will also benefit Deputy General Managers (DGMs) and Assistant General Managers (AGMs). With this change, the total CGM posts across the eleven banks will rise from 80 to 144, GM posts from 440 to 576, DGM posts from 1320 to 1728, and AGM posts from 3960 to 5184. This move addresses demands from banks and supports their growth in business and branch expansions.

Financial Inclusion Schemes

1. Pradhan Mantri Jan Dhan Yojana (PMJDY)

Pradhan Mantri Jan Dhan Yojana (PMJDY) was launched as the National Mission for Financial Inclusion on 28.8.2014. It aimed to ensure comprehensive financial inclusion of all households in the country by providing universal access to banking facilities with at least one basic bank account to every household, financial literacy, and social security cover.

The scheme offers:

- To unbanked persons a basic bank account without any minimum balance requirement, called a Basic Savings Bank Deposit (BSBD) account

- Free RuPay debit card, with in-built accident insurance cover of Rs. 2 lakh

- Access to overdraft facility of up to Rs. 10,000, subject to eligibility conditions

- Easy access to banking services in rural areas, through Bank Mitras

- Awareness about financial products through financial literacy programs

Progress under PMJDY (as on 20.11.2024):

- PMJDY Accounts: 54.03 crore

- Deposit in accounts: Rs 2,37,575 crore

- Women accounts: 30.07 crore (55.7%)

- Accounts in Rural/Semi urban: 35.95 crore (66.6%)

- RuPay cards issued: 36.92 crore

- Pradhan Mantri Suraksha Bima Yojana (PMSBY)

The Pradhan Mantri Suraksha Bima Yojana (PMSBY) is a one-year personal accident insurance scheme, renewable from year to year, offering coverage for death/disability due to an accident and is available to people in the age group of 18 to 70 years having a bank account who give their consent to join and enable auto-debit

- Annual premium is Rs 20 per year

- Risk Cover period: 1st June to 31st May

- Benefit of Rs. 2 Lakh payable on death or permanent total disability and Rs. 1 Lakh on partial disability. Simple claim settlement procedure / process involving minimum documentation put in place.

- It involves convenient bank account linked enrolment with implementation in IT mode, and premium payment through auto-debit from the bank account of the subscriber.

Progress under PMSBY (as on 20.11.2024):

- Cumulative enrolment: 47.59 crore

- Cumulative No. of Claims received: 1,93,964

- Cumulative No. of Claims disbursed: 1,47,641 for Rs. 2,931.88 crore

- Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY)

The Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY) is a one-year life insurance scheme, renewable from year to year, offering coverage of Rs. Two lacs for death due to any reason and is available to people in the age group of 18 to 50 years having a bank account.

- Annual premium is Rs.436 per year

- Risk Cover period: 1st June to 31st May

- It involves convenient bank account linked enrolment and premium payment through auto-debit from the bank account of the subscriber.

Progress under PMJJBY (as on 20.11.2024):

- Cumulative enrolment: 21.67 crore

- Cumulative No. of Claims received: 8,93,277

- Cumulative No. of Claims disbursed: 8,60,575 for Rs. 17,211.50 crore

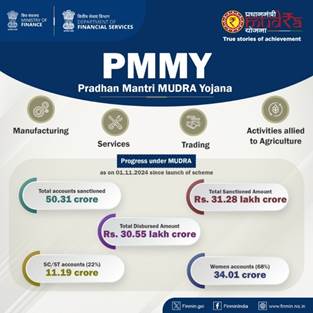

- Pradhan Mantri MUDRA Yojana (PMMY)

The Prime Minister launched Pradhan Mantri MUDRA Yojana (PMMY) on 08.04.2015 with an objective of providing access to institutional collateral free credit to micro enterprises up to Rs.10 lakh.

Features:

- Purposes: Non-agricultural, including activities allied to agriculture such as poultry, dairy, beekeeping etc. Term loan and working capital requirements can both be met

- Categories: Shishu – up to Rs.50,000, Kishore –Rs.50,000 to Rs.5 lakh, Tarun – Rs. 5 lakh to Rs.10 lakh

- Member Lending Institutions (MLIs): Public Sector Banks (PSBs), Private Sector Banks, Foreign Banks, Regional Rural Banks, Small Finance Banks, Non-Banking Financial Companies (NBFCs), Micro Finance Institutions (MFIs) and NBFC- MFIs.

- Collateral not required

- CGFMU Corpus available as on June 30th, 2024 (₹ in crore) = Rs. 5,106.94 Cr

Progress under MUDRA (as on 01.11.2024 since launch of scheme)

- Total accounts sanctioned: 50.31 crore

- SC/ST accounts:11.19 crore (22%)

- Women accounts: 34.01 crore (68%)

- Total Sanctioned Amount: Rs 31.28 lakh crore

- Total Disbursed Amount: Rs 30.55 lakh crore

- Stand Up India Scheme (SUPI)

- The Stand-up India Scheme was launched on 5th April 2016 to promote entrepreneurship among the Scheduled Caste/ Scheduled tribe and Women.

- Composite Loan between Rs.10 lakh and Rs. 1 crore to entrepreneurs above 18 years of age, through Scheduled Commercial Banks (SCBs).

- Loan between Rs.10 lakh and Rs. 1 crore through Scheduled Commercial Banks (SCBs).

- For setting up greenfield projects in manufacturing, services or trading sector and activities allied to agriculture.

- Repayment of the loan in a span of up to seven years including moratorium period of 18 months.

- Margin money ‘up to 15%’ which can be provided in convergence with eligible central/state government schemes. In any case, the borrower has to bring in minimum of 10 % of the project cost as his/her own contribution.

- Online portal www.standupmitra.in is providing guidance to prospective entrepreneurs in their endeavor to set up business enterprises, starting from training to filling up loan applications, as per bank requirements. In addition, one can also apply the loan over www.jansamarth.in portal.

Progress under Stand-Up India (as on 30.11.2024 since launch of scheme)

- Accounts sanctioned: 2.52 lakh

- Amount Sanctioned: Rs 56,975 crore

- Amount Disbursed: Rs 30,587 crore

- Women accounts: 1.91 lakh (76%)

6. Atal Pension Yojana

- APY was launched on 9th May, 2015 by the Hon’ble Prime Minister.

- APY is open to all Indian citizens having savings bank account / post office savings bank account in the age group of 18 to 40 years and the contributions differ, based on pension amount chosen. From 1st October,2022, any citizen who is or has been an income-tax payer, are not eligible to join APY.

- Subscribers would receive the guaranteed minimum monthly pension of Rs. 1000 or Rs. 2000 or Rs. 3000 or Rs. 4000 or Rs. 5000 at the age of 60 years.

- Under APY, the monthly pension would be available to the subscriber, and after him to his spouse and after their death, the pension corpus, as accumulated at age 60 of the subscriber, would be returned to the nominee of the subscriber.

- The minimum pension would be guaranteed by the Government, i.e., if the accumulated corpus based on contributions earns a lower than estimated return on investment and is inadequate to provide the minimum guaranteed pension, the Central Government would fund such inadequacy. Alternatively, if the returns on investment are higher, the subscribers would get enhanced pensionary benefits.

- As on 2nd December, 2024 a total of 7.11 crore subscribers have been enrolled under the Scheme.

- Females constitute around 47% of the total subscribers enrolled under the Scheme.

Progress under APY during last 8 years

|

|

31.3.17 |

31.3.18 |

31.3.19 |

31.3.20 |

31.3.21 |

31.3.22 |

31.3.23 |

31.3.2024

|

|

Subscribers enrolled (cumulative Fig .in lakh) |

48.83 |

97.05 |

154.18 |

223.01 |

302.15 |

401.27 |

520.58 |

643.52 |

NPS-Vatsalya

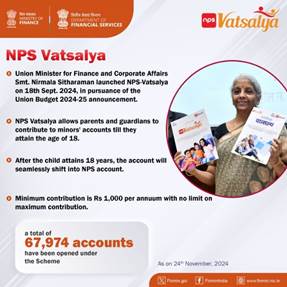

- The Finance Minister has launched the NPS-Vatsalya scheme on 18th September 2024 as a plan that allows parents and guardians to contribute to minors' accounts.

- Any minor who is a Citizen of India is eligible for opening account under the scheme, until attaining the age of eighteen years.

- Upon attainment of 18 years of age, the account of the subscriber shall continue to be operational and will be seamlessly shifted into NPS-Tier 1 Account- All Citizen Model.

- The minimum contribution is Rs 1000 per annuum and there shall be no limit on maximum contribution. The initial contribution for enrollment under the scheme is Rs 1000.

- In the case of death of the minor subscriber, the entire accumulated pension wealth to be paid to the guardian.

- The Finance Minister has announced the NPS-Vatsalya scheme in the Union Budget 2024-25 as a plan that allows parents and guardians to contribute to minors' accounts.

- Upon reaching the age of majority, these accounts can be seamlessly converted into normal NPS accounts.

- The Scheme has been launched on 18th September 2024.

- Opening an ‘NPS-Vatsalya’ account provides the child with a head start on saving for retirement and offers valuable financial lessons from an early age to reap the benefits of compounding in the later years.

- As on 24th November 2024, a total of 67,974 accounts have been opened under the Scheme.

Bima Sakhi Yojana launched

The Prime Minister launched the Bima Sakhi Yojana from Panipat on 9th December 2024. The ‘Bima Sakhi Yojana’ initiative of Life Insurance Corporation of India (LIC) is designed to empower women aged 18-70 years, who are Class X pass. It is a Stipendiary Scheme, exclusively for Women , with a stipendiary period of 3 years. Bima Sakhis will receive specialized training and a stipend for the first three years to promote financial literacy and insurance awareness. After training, they can serve as LIC agents and the graduate Bima Sakhis would have the opportunity to qualify for being considered for Development Officer roles in LIC.

Ground Level Agriculture Credit (GLC)

- It has been constant endeavor of the Government to boost agriculture sector through effective and hassle-free credit, for which the Government sets GLC targets for agriculture sector.

- The average achievement under agriculture credit during the last 5 years (FY 2019-20 to FY 2023-24) has been nearly 113% of the target and during this period GLC has grown at an average annual growth rate of 15.22%.

- During 2023–24, the growth in agriculture credit has remained robust, with a disbursement level of Rs. 25.49 lakh crore against the target of Rs. 20 lakh crore (127% achievement).

- During the period of FY 2019-20 to FY 2023-24, the share of small and Marginal farmers in agri credit disbursement (amount) has increased from 51.9% to 56.5% and share of small and marginal farmers as % of total accounts has increased from 74.97% to 76.42%.

- Keeping in view the past trend of credit disbursement and need for capital formation, Government has fixed GLC target of Rs. 27.50 lakh crore for FY2024-25.

- The target for GLC in agriculture has more than doubled from Rs. 13.5 lakh crore in FY 2019-20 to Rs. 27.5 lakh crore in FY 2024-25.

- In order to ensure increased credit flow to Animal Husbandry, Dairy & Fisheries activities a sub-target of Rs. 4.20 lakh crore has been fixed for these activities within the overall credit target of Rs. 27.50 lakh crore.

(In Rs. Crore)

|

FY |

Overall GLC Target |

Overall GLC Achievement |

Target for Allied Activities |

Achievement for Allied Activities |

|

2019-20 |

13,50,000 |

13,92,729 |

- |

- |

|

2020-21 |

15,00,000 |

15,75,398 |

- |

- |

|

2021-22 |

16,50,000 |

18,63,363 |

61,650 |

1,29,453 |

|

2022-23 |

18,50,000 |

21,55,163 |

1,26,000 |

2,61,538 |

|

2023-24 |

20,00,000 |

25,48,635 |

2,93,000 |

2,81,323 |

|

2024-25* |

27,50,000 |

10,56,942 |

4,20,000 |

1,38,106 |

*Data for FY 2024-25 is provisional as on 30.09.2024

Kisan Credit Card (KCC)

- Introduced in 1998, Kisan Credit Card (KCC) is a lending product issued to farmers for purchase of agriculture inputs such as seeds, fertilizers, pesticides etc. and to draw cash for crop production and allied activities

- Interest Subvention Scheme (ISS) was introduced in 2006 to provide short-term agriculture credit to farmers at subsidised rate.

- Modified Interest Subvention Scheme (MISS) with modification in IS was introduced in March 2022, under which short-term agriculture loan upto Rs. 3 lakh at 7% p.a. is provided. Interest Subvention (IS) of currently 1.5% is provided to banks for lending loans to farmers at 7%.

- Prompt Repayment Incentive (PRI) (currently at 3%) is also given to farmers for timely repayment of loans. Therefore, the effective interest rate for farmers is 4%.

- KCC facility was extended to Animal Husbandry and Fisheries farmers for their working requirement with interest subvention benefits up to Rs. 2 lakh under overall limit of Rs. 3 lakh in the year 2019.

- KCC loans upto the limit of Rs.1.6 lakh are extended collateral free.

- Total number of operative KCC Accounts as on September 2024 are 7.72 crore with total outstanding amount of Rs. 9.99 lakh crore.

- The details of KCC operative accounts and amount outstanding is placed below:

(No of Operative KCCs in actuals & Amount outstanding in Rs. Crore)

|

As on date |

No. of Operative Accounts |

Amount Outstanding |

|

31.03.2020 |

6,52,80,254 |

7,43,573 |

|

31.03.2021 |

7,37,45,010 |

7,53,431 |

|

31.03.2022 |

7,14,90,107 |

8,15,314 |

|

31.03.2023 |

7,34,70,282 |

8,85,464 |

|

31.03.2024 |

7,75,04,234 |

9,81,763 |

|

30.09.2024(current FY) |

7.72 crore |

9.99 lakh crore |

- In order to provide KCC to all eligible farmers Government of India had launched KCC Saturation Drive under Atma Nirbhar Bharat Abhiyan.

- Further, to expand the benefits of the Kisan Credit Card (KCC) to all eligible farmers engaged in Animal Husbandry, Dairy, and Fisheries(AHDF) activities Department of Animal Husbandry and Dairying and Department of Fisheries, in association with the Department of Financial Services, launched a nationwide district level weekly camps on 15.11.2021.

- The campaign has been extended from time to time latest being from 15.09.2024 to 31.03.2025.

- More than 37.64 lakh KCC applications for AHDF farmers have been sanctioned under this special saturation drive as on 27.09.2024.

- As a result of sustained and concerted efforts by the banks and other stakeholders in the direction of providing access to concessional credit to the farmers, total number of operative KCC Accounts for Animal Husbandry, Dairying and Fisheries (AHDF) have increased from 15.69 lakh as on 31.03.2022 to 45.65 lakh as on 30.06.2024 and outstanding amount under AHDF has increased from Rs. 16,747 crore to Rs. 54,253 crore during this period.

****

NB/KMN

(Release ID: 2088182)