Ministry of Finance

SUMMARY OF THE UNION BUDGET 2024-2025

Posted On: 23 JUL 2024

PART A

Despite global economy remaining under the grip of policy uncertainties, India’s economic growth continues to be the shining exception and will remain so in the years ahead. Minister of Finance and Corporate Affairs Smt Nirmala Sitharaman, while presenting the Union Budget 2024-25 in Parliament today said that India’s inflation continues to be low, stable and moving towards the 4 per cent target. Core inflation (non-food, non-fuel) currently is 3.1 per cent and steps are being taken to ensure supplies of perishable goods reach market adequately.

Interim Budget

The Finance Minister said that as mentioned in the interim budget, the focus is on 4 major castes, namely ‘Garib’ (Poor), ‘Mahilayen’ (Women), ‘Yuva’ (Youth) and ‘Annadata’ (Farmer).

Budget Theme

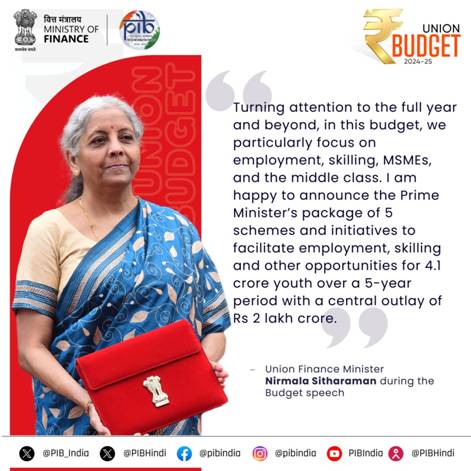

Dwelling on the Budget theme, Smt Sitharaman said, turning attention to the full year and beyond, in this budget, we particularly focus on employment, skilling, MSMEs, and the middle class. She announced the Prime Minister’s package of 5 schemes and initiatives to facilitate employment, skilling and other opportunities for 4.1 crore youth over a 5-year period with a central outlay of ₹2 lakh crore. This year, ₹1.48 lakh crore has been allocated for education, employment and skilling.

Budget Priorities

The Finance Minister said, for pursuit of ‘Viksit Bharat’, the budget envisages sustained efforts on the following 9 priorities for generating ample opportunities for all.

- Productivity and resilience in Agriculture

- Employment & Skilling

- Inclusive Human Resource Development and Social Justice

- Manufacturing & Services

- Urban Development

- Energy Security

- Infrastructure

- Innovation, Research & Development and

- Next Generation Reforms

Priority 1: Productivity and resilience in Agriculture

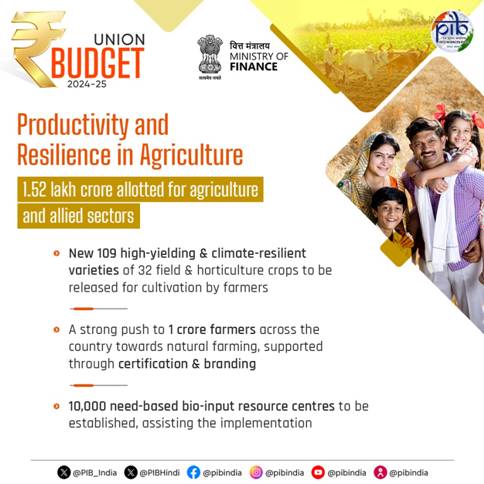

The Finance Minister announced that the government will undertake a comprehensive review of the agriculture research setup to bring the focus on raising productivity. New 109 high-yielding and climate-resilient varieties of 32 field and horticulture crops will be released for cultivation by farmers.

In the next two years, 1 crore farmers across the country will be initiated into natural farming supported by certification and branding.

10,000 need-based bio-input resource centres will be established.

For achieving self-sufficiency in pulses and oilseeds, government will strengthen their production, storage and marketing and to achieve ‘atmanirbharta’ for oil seeds such as mustard, groundnut, sesame, soybean, and sunflower.

Government, in partnership with the states, will facilitate the implementation of the Digital Public Infrastructure (DPI) in agriculture for coverage of farmers and their lands in 3 years.

Smt Sitharaman announced a provision of ₹1.52 lakh crore for agriculture and allied sector this year.

Priority 2: Employment & Skilling

The Finance Minister said that the government will implement 3 schemes for ‘Employment Linked Incentive’, as part of the Prime Minister’s package. These will be based on enrolment in the EPFO, and focus on recognition of first-time employees, and support to employees and employers.

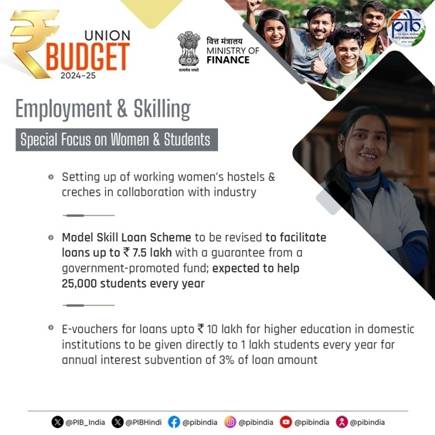

Government will also facilitate higher participation of women in the workforce through setting up of working women hostels in collaboration with industry, and establishing creches.

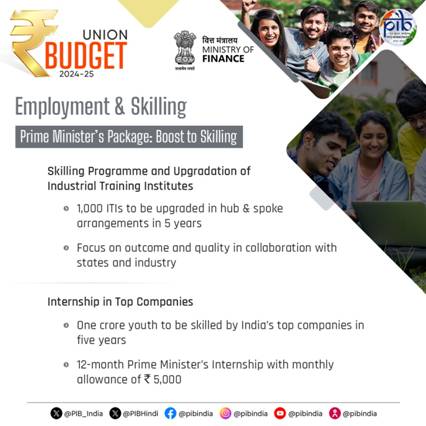

Referring to the Skilling programme, the Finance Minister announced a new centrally sponsored scheme, as the 4th scheme under the Prime Minister’s package, for skilling in collaboration with state governments and Industry. 20 lakh youth will be skilled over a 5-year period and 1,000 Industrial Training Institutes will be upgraded in hub and spoke arrangements with outcome orientation.

She also announced that the Model Skill Loan Scheme will be revised to facilitate loans up to

₹7.5 lakh with a guarantee from a government promoted Fund, which is expected to help 25,000 students every year.

For helping the youth, who have not been eligible for any benefit under government schemes and policies, she announced a financial support for loans upto ₹10 lakh for higher education in domestic institutions. E-vouchers for this purpose will be given directly to 1 lakh students every year for annual interest subvention of 3 per cent of the loan amount.

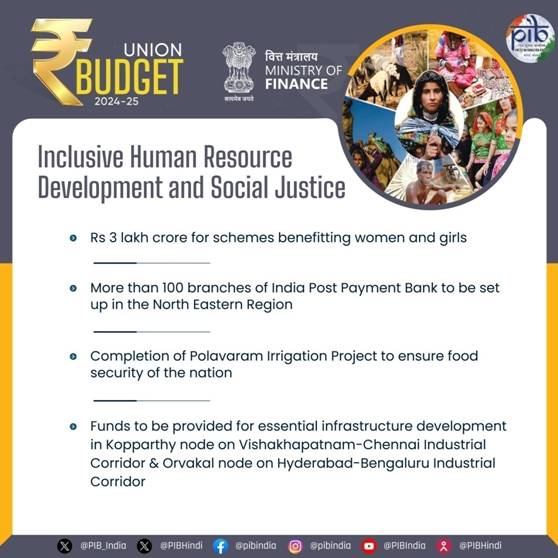

Priority 3: Inclusive Human Resource Development and Social Justice

Talking about the Saturation approach, the Finance Minister emphasised that implementation of schemes meant for supporting economic activities by craftsmen, artisans, self-help groups, scheduled caste, schedule tribe and women entrepreneurs, and street vendors, such as PM Vishwakarma, PM SVANidhi, National Livelihood Missions, and Stand-Up India will be stepped up.

Purvodaya

Government will formulate a plan, Purvodaya, for the all-round development of the eastern region of the country covering Bihar, Jharkhand, West Bengal, Odisha and Andhra Pradesh. This will cover human resource development, infrastructure, and generation of economic opportunities to make the region an engine to attain Viksit Bharat.

Pradhan Mantri Janjatiya Unnat Gram Abhiyan

The Finance Minister announced that for improving the socio-economic condition of tribal communities, government will launch the Pradhan Mantri Janjatiya Unnat Gram Abhiyan by adopting saturation coverage for tribal families in tribal-majority villages and aspirational districts covering 63,000 villages and benefitting 5 crore tribal people.

More than 100 branches of India Post Payment Bank will be set up in the North East region to expand the banking services.

She said, a provision of ₹2.66 lakh crore for rural development including rural infrastructure was made this year.

Priority 4: Manufacturing & Services

Support for promotion of MSMEs

Smt Sitharaman said, this budget provides special attention to MSMEs and manufacturing, particularly labour-intensive manufacturing. A separately constituted self-financing guarantee fund will provide, to each applicant, guarantee cover up to ₹100 crore, while the loan amount may be larger. Similarly, Public sector banks will build their in-house capability to assess MSMEs for credit, instead of relying on external assessment. She also announced a new mechanism for facilitating continuation of bank credit to MSMEs during their stress period.

Mudra Loans

The limit of Mudra loans will be enhanced to ₹ 20 lakh from the current ₹ 10 lakh for those entrepreneurs who have availed and successfully repaid previous loans under the ‘Tarun’ category.

MSME Units for Food Irradiation, Quality & Safety Testing

Financial support for setting up of 50 multi-product food irradiation units in the MSME sector will be provided. Setting up of 100 food quality and safety testing labs with NABL accreditation will also be facilitated. To enable MSMEs and traditional artisans to sell their products in international markets, E-Commerce Export Hubs will be set up in public-private-partnership (PPP) mode .

Internship in Top Companies

The Finance Minister said that as the 5th scheme under the Prime Minister’s package, government will launch a comprehensive scheme for providing internship opportunities in 500 top companies to 1 crore youth in 5 years.

Priority 5: Urban Development

Urban Housing

Under the PM AwasYojana Urban 2.0, housing needs of 1 crore urban poor and middle-class families will be addressed with an investment of ₹ 10 lakh crore. This will include the central assistance of ₹ 2.2 lakh crore in the next 5 years.

Water Supply and Sanitation

In partnership with the State Governments and Multilateral Development Banks, government will promote water supply, sewage treatment and solid waste management projects and services for 100 large cities through bankable projects.

PM SVANidhi

She added that building on the success of PM SVANidhi Scheme in transforming the lives of street vendors, Government envisions a scheme to support each year, over the next five years, the development of 100 weekly ‘haats’ or street food hubs in select cities.

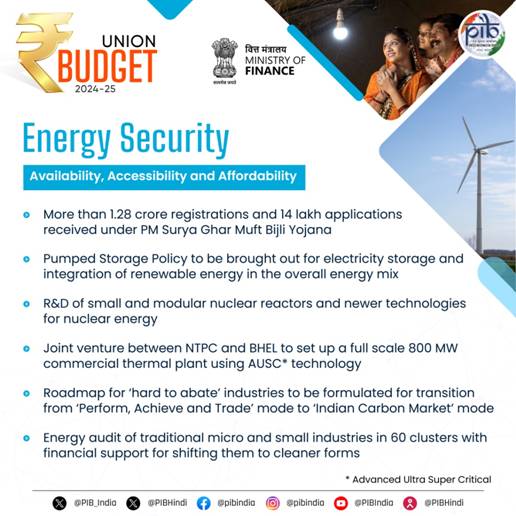

Priority 6: Energy Security

The Finance Minister said, in line with the announcement in the interim budget, PM Surya Ghar Muft Bijli Yojana has been launched to install rooftop solar plants to enable 1 crore households obtain free electricity up to 300 units every month. The scheme has generated remarkable response with more than 1.28 crore registrations and 14 lakh applications.

Nuclear energy is expected to form a very significant part of the energy mix for Viksit Bharat.

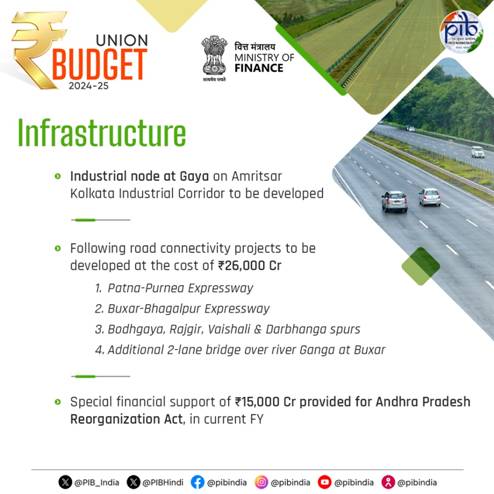

Priority 7: Infrastructure

The Finance Minister underlined that significant investment the Central Government has made over the years in building and improving infrastructure has had a strong multiplier effect on the economy. Government will endeavour to maintain strong fiscal support for infrastructure over the next 5 years, in conjunction with imperatives of other priorities and fiscal consolidation. ₹11,11,111 crore for capital expenditure has been allocated this year, which is 3.4 per cent of our GDP.

Pradhan Mantri Gram SadakYojana (PMGSY)

The Finance Minister announced that Phase IV of PMGSY will be launched to provide all-weather connectivity to 25,000 rural habitations which have become eligible in view of their population increase.

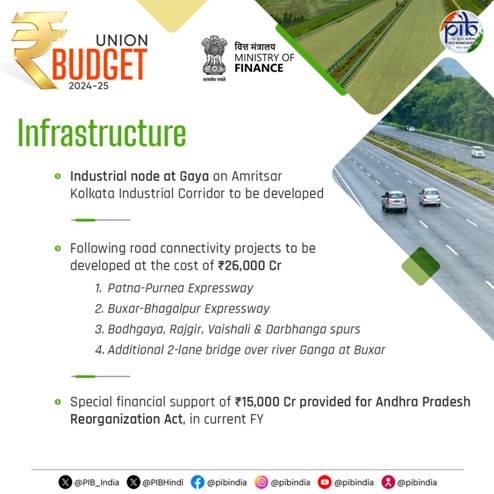

For Irrigation and Flood Mitigation in Bihar, through the Accelerated Irrigation Benefit Programme and other sources, government will provide financial support for projects with estimated cost of ₹11,500 crore such as the Kosi-Mechi intra-state link and 20 other ongoing and new schemes including barrages, river pollution abatement and irrigation projects. Government will also provide assistance to Assam, Himachal Pradesh, Uttarakhand and Sikkim for flood management, landslides and related projects.

Priority 8: Innovation, Research & Development

The Finance Minister said that government will operationalize the Anusandhan National Research Fund for basic research and prototype development and set up a mechanism for spurring private sector-driven research and innovation at commercial scale with a financing pool of ₹1 lakh crore in line with the announcement in the interim budget.

Space Economy

With our continued emphasis on expanding the space economy by 5 times in the next 10 years, a venture capital fund of ₹1,000 crore will be set up.

Priority 9: Next Generation Reforms

Economic Policy Framework

The Finance Minister said that the government will formulate an Economic Policy Framework to delineate the overarching approach to economic development and set the scope of the next generation of reforms for facilitating employment opportunities and sustaining high growth.

Labour related reforms

Government will facilitate the provision of a wide array of services to labour, including those for employment and skilling. A comprehensive integration of e-shram portal with other portals will facilitate such one-stop solution. Shram Suvidha and Samadhan portals will be revamped to enhance ease of compliance for industry and trade.

Government will develop a taxonomy for climate finance for enhancing the availability of capital for climate adaptation and mitigation.

Foreign Direct Investment and Overseas Investment

The rules and regulations for Foreign Direct Investment and Overseas Investments will be simplified to (1) facilitate foreign direct investments, (2) nudge prioritization, and (3) promote opportunities for using Indian Rupee as a currency for overseas investments.

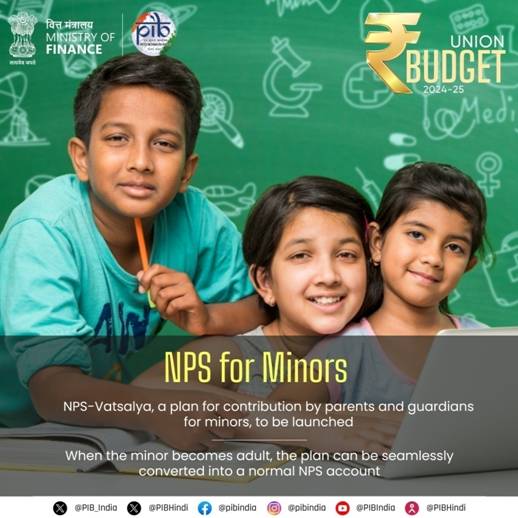

NPS Vatsalya

NPS-Vatsalya, a plan for contribution by parents and guardians for minors will be started. On attaining the age of majority, the plan can be converted seamlessly into a normal NPS account.

New Pension Scheme (NPS)

The Finance Minister said that the Committee to review the NPS has made considerable progress in its work and a solution will be evolved which addresses the relevant issues while maintaining fiscal prudence to protect the common citizens.

Budget Estimates 2024-25

The Finance Minister informed that for the year 2024-25, the total receipts other than borrowings and the total expenditure are estimated at ₹32.07 lakh crore and ₹48.21 lakh crore respectively. The net tax receipts are estimated at ₹25.83 lakh crore and the fiscal deficit is estimated at 4.9 per cent of GDP.

She said, the gross and net market borrowings through dated securities during 2024-25 are estimated at ₹14.01 lakh crore and ₹11.63 lakh crore respectively.

Smt Sitharaman emphasised that the fiscal consolidation path announced by her in 2021 has served economy very well, and the government will aim to reach a deficit below 4.5 per cent next year.

PART B

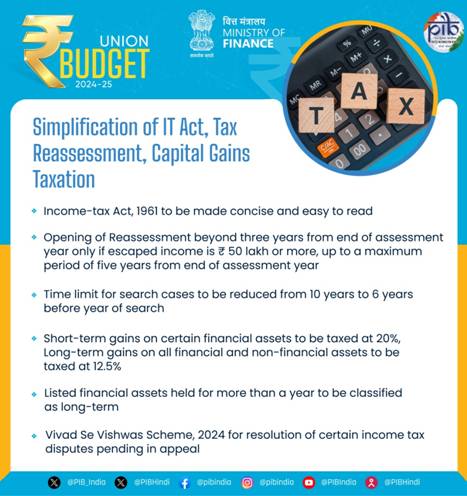

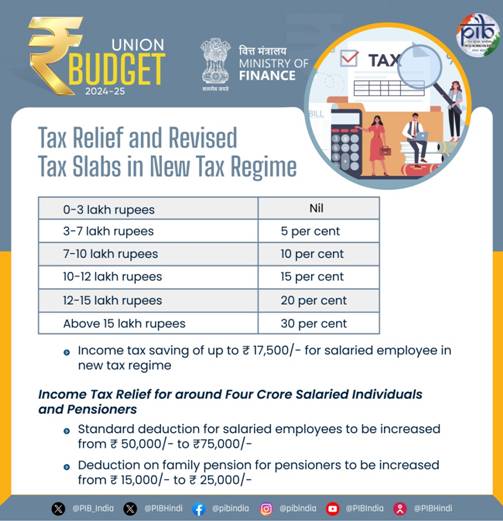

Apart from giving relief to four crore salaried individuals and pensioners of the country in the direct taxes, Union Budget 2024-25 seeks to comprehensively review the direct and indirect taxes in the next six months, simplifying them, reducing tax incidence and compliance burdens and broadening the tax nets. The Budget proposes comprehensive rationalization of GST tax structure along with review of the Custom Duty rate structure to improve the tax base and support domestic manufacturing. A comprehensive review of Income – Tax Act is targeted at reducing disputes and litigations and to make the act lucid, concise and easy to read. Minister of Finance and Corporate Affairs Smt. Nirmala Sitharaman said that simplification of tax regimes without exemptions and deductions for corporate and personal income tax has been appreciated by tax payers as over 58 per cent of corporate tax came from simplified tax regime in 2022-23 and more than two third tax payers have switched over to the new personal income tax regime.

Budget 2024-25 increased standard deduction of salaried employees from ₹ 50,000/- to ₹ 75,000/- for those opting for new tax regime. Similarly, deduction on family pension for pensioners enhanced from ₹ 15,000/- to ₹ 25,000/-. Assessments now, can be reopened beyond three years up to 5 years from end of year of assessment, only if, the escaped income is more than ₹ 50 Lakh. The new tax regime rate structure is also revised to give a salaried employee benefits up to ₹ 17,500/- in income tax.

|

Income Slabs |

Tax Rate |

|

0 – 3 Lakh rupees |

NIL |

|

3 – 7 Lakh rupees |

5 per cent |

|

7 – 10 Lakh rupees |

10 per cent |

|

10 – 12 Lakh rupees |

15 per cent |

|

12 – 15 Lakh rupees |

20 per cent |

|

Above 15 Lakh rupees |

30 per cent |

Table 1: New Tax Regime Tax Structure

To promote investment and foster employment, Budget has given boost to entrepreneurial spirit and start-up ecosystem, abolishing angel tax for all classes of investors. Further, a simpler tax regime for foreign shipping companies operating domestic cruises is proposed looking at the tremendous potential of cruise tourism. Foreign mining companies selling raw diamonds in the country can now benefit from safe harbor rates which will benefit the diamond industry. Further, corporate tax rate on foreign companies reduced from 40 to 35 per cent to attract foreign capital.

Budget further simplified the direct tax regime for charities, TDS rate structure and capital gains taxation. The two tax exemption regimes for charities will be merged into one. 5 per cent TDS on many payments to be merged into 2 per cent TDS and 20 per cent TDS on repurchase of units by mutual funds or UTI stands withdrawn. TDS rate on e-commerce operators reduced from 1 per cent to 0.1 per cent. Now credit of TCS will be given on TDS deducted from salary. Budget decriminalized delay of payment of TDS up to the due date of filing of TDS statement. Standard Operating Procedure soon for simplified and rationalized compounding guidelines for TDS defaults.

On Capital gains, short term gains shall henceforth attract a rate of 20 per cent on certain financial assets. Long term gains on all financial and non-financial assets to attract 12.5 per cent rate. Limit of exemption of capital gains has been increased to ₹1.25 Lakh per year to benefit lower and middle-income classes. Listed financial assets held for more than a year and unlisted assets (financial and non-financial) held for more than two years to be classified as long term assets. Unlisted bonds and debentures, debt mutual funds and market linked debentures will continue to attract applicable capital gains tax.

Acknowledging that GST has decreased tax incidence on common man and terming it as a success of vast proportions, Union Finance Minister Smt Nirmala Sitharaman said that GST has reduced compliance burden and logistics cost for trade and industry. Now the Government envisages further simplifying and rationalizing the tax structure to expand it to remaining sectors. Budget also proposed to further digitalise and make paperless the remaining services of Customs and Income Tax including rectification and order giving effect to appellate orders over the next two years.

Custom duties have been revised to rationalize and revise them for ease of trade and reduction of disputes. Giving relief to cancer patients, Budget fully exempted three more cancer treating medicines from custom duties, namely, Trastuzumab Deruxtecan, Osimertinib and Durvalumab. There will be reduction in Basic Customs Duty (BCD) on X-ray machines tubes and flat panel detectors. BCD on mobile phones, Printed Circuit Board Assembly (PCBA) and mobile chargers reduced to 15 per cent. To give a fillip to processing and refining of critical minerals, Budget fully exempted custom duties on 25 rare earth minerals like lithium and reduced BCD on two of them. Budget proposed to exempt capital goods for manufacturing of solar panels. To boost India’s seafood exports, BCD on broodstock, polychaete worms, shrimps and fish feed reduced to 5 per cent. Budget will foster competitiveness of Indian leather and textiles articles of export. BCD reduced from 7.5 per cent to 5 per cent in Methylene Diphenyl Diisocyanate (MDI) used for manufacture of spandex yarn. Custom duties on gold and silver reduced to 6 per cent and on platinum to 6.4 per cent. BCD on ferro nickel and blister copper removed, while, BCD on ammonium nitrate increased from 7.5 to 10 per cent to support existing and new capacities in pipeline. Similarly, BCD on PVC flex banners increased from 10 to 25 per cent considering the hazard to environment. To incentivize domestic manufacturing, BCD on PCBA of specific telecom equipments increased from 10 to 15 per cent.

For dispute resolution and dispose-off backlogs, Union Finance Minister proposed Vivad se Vishwas Scheme, 2024 for resolsution of certain income tax disputes pending in appeal. The monetary limits for filing appeals related to direct taxes, excise and service tax in High Courts, Supreme Courts and tribunals has been increased to ₹ 60 Lakh, ₹ 2 Crore and ₹ 5 Crore, respectively. Further to reduce litigation and provide certainty in international taxation, scope of safe harbour rules to be expanded and transfer pricing assessment procedure to be streamlined.

*****

NB/SNC/VV/VC

(Release ID: 2035618)

Ministry of Finance

Union Budget 2024-25: Advancing Economic Growth through Infrastructure Initiatives

Posted On: 23 JUL 2024

The Union Minister of Finance and Corporate Affairs, Smt. Nirmala Sitharaman, presented the Union Budget 2024-25 in Parliament today. This budget envisions sustained efforts across nine key priorities to generate ample opportunities for all, in pursuit of ‘Viksit Bharat.’ The key priorities include Productivity and Resilience in Agriculture, Employment & Skilling, Inclusive Human Resource Development and Social Justice, Manufacturing & Services, Urban Development, Energy Security, Infrastructure, Innovation, Research & Development, and Next Generation Reforms. Among these, significant announcements have been made in relation to the infrastructure sector.

Infrastructure Development

The Finance Minister emphasized the significant investment the Central Government has made over the years in building and improving infrastructure, which has had a strong multiplier effect on the economy. The government will maintain strong fiscal support for infrastructure over the next five years, while balancing other priorities and fiscal consolidation. An allocation of ₹11,11,111 crore for capital expenditure, which is 3.4 percent of GDP, has been made this year.

The government will encourage states to provide similar scale support for infrastructure, aligning with their development priorities. A provision of ₹1.5 lakh crore for long-term interest-free loans has been made this year to assist states in their resource allocation. Investment in infrastructure by the private sector will be promoted through viability gap funding and supportive policies and regulations. A market-based financing framework will also be introduced.

Despite many financial innovations in infrastructure financing in the recent years, capital expenditure by the Union and State Governments still has the central role in funding of large-scale infrastructure projects. The capital expenditure of the Union Government increased by 2.2 times from FY21 to FY24 (PA) while that of the State governments increased by 2.1 times during the same period.

The net flow of funds to infrastructure sectors through bank credit between March 2023 to March 2024 was only around ₹79,000 crore, much less than the GBS by the Union Government for either railways or roads. The net flow of bank credit between March 2020 and March 2024 was concentrated in only a few sectors roads, airports and power. However, the credit growth to infrastructure sectors in FY24 recovered to 6.5 per cent, as against the growth of 2.3 per cent, in FY23.

The gross inflow of external commercial borrowings to infrastructure sectors also picked up to USD 9.05 billion in FY24, as against an average of USD 5.91 billion during FY20 to FY23. The resource mobilisation by infrastructure sectors through debt and equity issuances in the capital market was just over ₹1,00,000 crore during FY24. Real estate investment trusts REITs) have raised ₹18,840 crore from year 2019 to 2024 while Infrastructure investment trusts (InvITs) raised a total of ₹1,11,294 crore in the last five years (2019-2024).

Existing Mechanisms for Fostering Public Private Partnership (PPP)

- Public Private Partnership Appraisal Committee (PPPAC)

- Apex body for appraisal of central sector PPP projects.

- 77 projects with a total cost of ₹2.4 lakh crore were recommended from FY15 to FY24.

- Viability Gap Funding (VGF)

- Assistance to financially unviable but socially/economically desirable PPP projects.

- 57 projects costing ₹64,926. One crore was granted in-principle approval and 27 projects costing ₹25,263.8 crore were granted final approval from FY15 to FY24.

- Total VGF approval of ₹5,813.6 crore (both Union Government & State share) from FY15 to FY24.

- India Infrastructure Project Development Fund Scheme

- Financial support for project development of PPP Projects

- Notified in November 2022 with a total outlay of ₹150 crore for three years from FY23 to FY25.

- 28 proposals have been approved.

- National Monetisation Pipeline (NMP)

- NMP was announced in August 2021 on the principle of ‘asset creation through monetisation’ i.e., tapping private sector investment for new infrastructure creation.

- The aggregate monetisation potential under NMP was estimated at ₹6.0 lakh crore through core assets of the Government, over four-years from FY22 to FY25.

- Other Supportive instruments

- Reference guides for setting up state PPP units, PPP project appraisal, and project implementation mode selection have been made.

- Web-based toolkits, post-award contract management toolkit and contingent liability for project sponsoring authorities have been developed to help them in PPP structuring.

Pradhan Mantri Gram Sadak Yojana (PMGSY)

The Finance Minister in the Union budget announced that Phase IV of PMGSY will be launched to provide all-weather connectivity to 25,000 rural habitations which have become eligible in view of their population increase.

The Pradhan Mantri Gram Sadak Yojana, launched on 25th December 2000, aims to provide all-weather access to eligible unconnected habitations and is a 100% Centrally Sponsored Scheme. As of July 23, 2024, 8,10,083 km of road has been sanctioned, with 7,65,530 km completed. A total of ₹3,24,177 crore has been spent on this scheme.

Irrigation and Flood Mitigation

For irrigation and flood mitigation in Bihar, the government will provide financial support for projects with an estimated cost of ₹11,500 crore through the Accelerated Irrigation Benefit Programme and other sources. This includes the Kosi-Mechi intra-state link and 20 other ongoing and new schemes. The Union budget also announced assistance for flood management, landslides, and related projects in Assam, Himachal Pradesh, Uttarakhand, and Sikkim.

The Union Budget 2024-25 demonstrates a strong commitment to advancing infrastructure and economic growth. The continued emphasis on public-private partnerships and infrastructure investment reflects the government's vision of a ‘Viksit Bharat.’ With sustained efforts and strategic initiatives, India is well-positioned to achieve significant economic progress and development in the coming years.